![]()

Mortgage debtors

who’ve been holding out for decrease

rates of interest

at the moment are discovering they’ve run out of time, say business professionals.

Fastened-rate mortgages, that are influenced by market circumstances and authorities bond yields, have been drifting greater, rising from a spread of mid-3 per cent this fall to low 4 per cent now.

“Over the previous few months, I’ve seen purchasers flip down fixed-rate renewal affords round 3.7 per cent as a result of they have been satisfied charges would preserve falling,” stated Leah Zlatkin, a mortgage dealer and

LowestRates.ca

knowledgeable.

“Now those self same debtors are coming again and discovering that the most effective out there charges begin with a 4. That delay is already leading to greater month-to-month funds.”

By the top of 2026, greater than a 3rd of Canadian owners will renew their mortgages, lots of them at greater charges from the lows of the pandemic.

Over the previous 12 months, variable charges have dropped greater than fastened, from 7 per cent in June 2024 to barely under 4 per cent because the

Financial institution of Canada

minimize its benchmark charge.

Nevertheless, additional reduction on this entrance now seems to be unlikely with the central financial institution anticipated to maintain charges regular this 12 months or, as some consider, elevate them by 12 months finish.

In the meantime, fastened charges have fallen simply barely greater than 100 foundation factors, with five-year phrases lower than that.

Bond yields have been pushed greater just lately by the central financial institution’s determination to maintain charges on maintain and financial information beating expectations. They will also be influenced by inflation, public deficits and worldwide monetary circumstances.

As a result of fastened charges are dictated by market circumstances delays might result in greater somewhat than decrease charges, stated Zlatkin. And even a small enhance in a charge can add as much as greater month-to-month funds, particularly for owners with bigger mortgages.

One shocking development in Canada has been the decline in recognition of the five-year time period, a conventional desire, stated Hendrix Vachon, Desjardins Group principal economist, in a current report.

Earlier than the pandemic, about 30 per cent of recent financing was on a five-year or extra time period, however between 2022 and 2025 that share dropped to fifteen per cent, in response to information from the Financial institution of Canada.

The most well-liked mortgages now are fastened charge with phrases between three and 5 years, accounting for almost 40 per cent of mortgages, he stated.

Zlatkin stated selecting a shorter time period will help debtors safe at this time’s charges whereas leaving room to regulate if circumstances change.

Homebuyers must also take heed. Within the present purchaser’s market, negotiating a greater value will help offset mortgage charges, however timing nonetheless issues.

“Householders who worth predictable funds shouldn’t be ready for an ideal second,” she stated. “On this surroundings, ready can imply paying extra whereas gaining little or no in return.”

Enroll right here to get Posthaste delivered straight to your inbox.

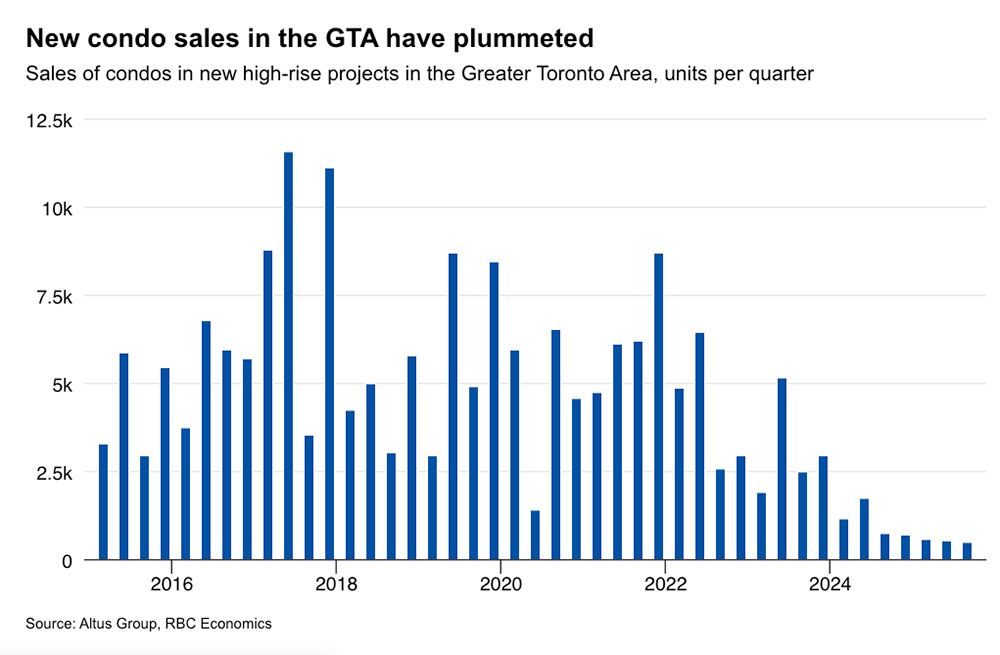

At the moment’s chart from

Royal Financial institution of Canada

provides us an image of simply how unhealthy Toronto’s rental market has grow to be. Pre-construction gross sales in 2025 have been down 90 per cent from the common over the 9 years earlier than 2024, stated RBC.

“The Higher Toronto Space’s new condominium improvement sector has entered a deep freeze with pre-construction gross sales plummeting to ranges not seen for the reason that international monetary disaster,” wrote Robert Hogue, RBC assistant chief economist, in a report in September.

This spells bother for housing development, stated the financial institution. It expects housing begins to fall greater than 10 per cent nationally in 2026 and much more in 2027, regardless of authorities efforts to bolster the nation’s housing provide.

- RBC Capital Markets holds Canadian financial institution CEO convention in Toronto

- Vancouver dwelling gross sales

- How Edward Rogers and Tony Staffieri gained 2025 and what they’ve deliberate for an encore

- Three under-the-radar dangers Canadian buyers ought to concentrate on this 12 months

- Why Caisse CEO Charles Emond thinks Canada is near getting the infrastructure formulation proper

Ought to Margaret, 62, purchase a rental or beef up her investments together with her $275,000 inheritance? Discover out why FP Solutions thinks on this case renting is probably not a foul alternative.

Learn extra

![]()

Considering vitality? The subscriber-only FP West: Vitality Insider e-newsletter brings you unique reporting and in-depth evaluation on one of many nation’s most essential sectors.

Enroll right here.

McLister on mortgages

Wish to be taught extra about mortgages? Mortgage strategist Robert McLister’s

Monetary Publish column

will help navigate the advanced sector, from the newest tendencies to financing alternatives you gained’t wish to miss. Plus verify his

mortgage charge web page

for Canada’s lowest nationwide mortgage charges, up to date every day.

Monetary Publish on YouTube

Go to the Monetary Publish’s

YouTube channel

for interviews with Canada’s main consultants in enterprise, economics, housing, the vitality sector and extra.

At the moment’s Posthaste was written by Pamela Heaven with further reporting from Monetary Publish workers, The Canadian Press and Bloomberg.

Have a narrative concept, pitch, embargoed report, or a suggestion for this article? Electronic mail us at

.

Bookmark our web site and help our journalism: Don’t miss the enterprise information that you must know — add financialpost.com to your bookmarks and join our newsletters right here

![]()

Mortgage debtors

who’ve been holding out for decrease

rates of interest

at the moment are discovering they’ve run out of time, say business professionals.

Fastened-rate mortgages, that are influenced by market circumstances and authorities bond yields, have been drifting greater, rising from a spread of mid-3 per cent this fall to low 4 per cent now.

“Over the previous few months, I’ve seen purchasers flip down fixed-rate renewal affords round 3.7 per cent as a result of they have been satisfied charges would preserve falling,” stated Leah Zlatkin, a mortgage dealer and

LowestRates.ca

knowledgeable.

“Now those self same debtors are coming again and discovering that the most effective out there charges begin with a 4. That delay is already leading to greater month-to-month funds.”

By the top of 2026, greater than a 3rd of Canadian owners will renew their mortgages, lots of them at greater charges from the lows of the pandemic.

Over the previous 12 months, variable charges have dropped greater than fastened, from 7 per cent in June 2024 to barely under 4 per cent because the

Financial institution of Canada

minimize its benchmark charge.

Nevertheless, additional reduction on this entrance now seems to be unlikely with the central financial institution anticipated to maintain charges regular this 12 months or, as some consider, elevate them by 12 months finish.

In the meantime, fastened charges have fallen simply barely greater than 100 foundation factors, with five-year phrases lower than that.

Bond yields have been pushed greater just lately by the central financial institution’s determination to maintain charges on maintain and financial information beating expectations. They will also be influenced by inflation, public deficits and worldwide monetary circumstances.

As a result of fastened charges are dictated by market circumstances delays might result in greater somewhat than decrease charges, stated Zlatkin. And even a small enhance in a charge can add as much as greater month-to-month funds, particularly for owners with bigger mortgages.

One shocking development in Canada has been the decline in recognition of the five-year time period, a conventional desire, stated Hendrix Vachon, Desjardins Group principal economist, in a current report.

Earlier than the pandemic, about 30 per cent of recent financing was on a five-year or extra time period, however between 2022 and 2025 that share dropped to fifteen per cent, in response to information from the Financial institution of Canada.

The most well-liked mortgages now are fastened charge with phrases between three and 5 years, accounting for almost 40 per cent of mortgages, he stated.

Zlatkin stated selecting a shorter time period will help debtors safe at this time’s charges whereas leaving room to regulate if circumstances change.

Homebuyers must also take heed. Within the present purchaser’s market, negotiating a greater value will help offset mortgage charges, however timing nonetheless issues.

“Householders who worth predictable funds shouldn’t be ready for an ideal second,” she stated. “On this surroundings, ready can imply paying extra whereas gaining little or no in return.”

Enroll right here to get Posthaste delivered straight to your inbox.

At the moment’s chart from

Royal Financial institution of Canada

provides us an image of simply how unhealthy Toronto’s rental market has grow to be. Pre-construction gross sales in 2025 have been down 90 per cent from the common over the 9 years earlier than 2024, stated RBC.

“The Higher Toronto Space’s new condominium improvement sector has entered a deep freeze with pre-construction gross sales plummeting to ranges not seen for the reason that international monetary disaster,” wrote Robert Hogue, RBC assistant chief economist, in a report in September.

This spells bother for housing development, stated the financial institution. It expects housing begins to fall greater than 10 per cent nationally in 2026 and much more in 2027, regardless of authorities efforts to bolster the nation’s housing provide.

- RBC Capital Markets holds Canadian financial institution CEO convention in Toronto

- Vancouver dwelling gross sales

- How Edward Rogers and Tony Staffieri gained 2025 and what they’ve deliberate for an encore

- Three under-the-radar dangers Canadian buyers ought to concentrate on this 12 months

- Why Caisse CEO Charles Emond thinks Canada is near getting the infrastructure formulation proper

Ought to Margaret, 62, purchase a rental or beef up her investments together with her $275,000 inheritance? Discover out why FP Solutions thinks on this case renting is probably not a foul alternative.

Learn extra

![]()

Considering vitality? The subscriber-only FP West: Vitality Insider e-newsletter brings you unique reporting and in-depth evaluation on one of many nation’s most essential sectors.

Enroll right here.

McLister on mortgages

Wish to be taught extra about mortgages? Mortgage strategist Robert McLister’s

Monetary Publish column

will help navigate the advanced sector, from the newest tendencies to financing alternatives you gained’t wish to miss. Plus verify his

mortgage charge web page

for Canada’s lowest nationwide mortgage charges, up to date every day.

Monetary Publish on YouTube

Go to the Monetary Publish’s

YouTube channel

for interviews with Canada’s main consultants in enterprise, economics, housing, the vitality sector and extra.

At the moment’s Posthaste was written by Pamela Heaven with further reporting from Monetary Publish workers, The Canadian Press and Bloomberg.

Have a narrative concept, pitch, embargoed report, or a suggestion for this article? Electronic mail us at

.

Bookmark our web site and help our journalism: Don’t miss the enterprise information that you must know — add financialpost.com to your bookmarks and join our newsletters right here

![]()

Mortgage debtors

who’ve been holding out for decrease

rates of interest

at the moment are discovering they’ve run out of time, say business professionals.

Fastened-rate mortgages, that are influenced by market circumstances and authorities bond yields, have been drifting greater, rising from a spread of mid-3 per cent this fall to low 4 per cent now.

“Over the previous few months, I’ve seen purchasers flip down fixed-rate renewal affords round 3.7 per cent as a result of they have been satisfied charges would preserve falling,” stated Leah Zlatkin, a mortgage dealer and

LowestRates.ca

knowledgeable.

“Now those self same debtors are coming again and discovering that the most effective out there charges begin with a 4. That delay is already leading to greater month-to-month funds.”

By the top of 2026, greater than a 3rd of Canadian owners will renew their mortgages, lots of them at greater charges from the lows of the pandemic.

Over the previous 12 months, variable charges have dropped greater than fastened, from 7 per cent in June 2024 to barely under 4 per cent because the

Financial institution of Canada

minimize its benchmark charge.

Nevertheless, additional reduction on this entrance now seems to be unlikely with the central financial institution anticipated to maintain charges regular this 12 months or, as some consider, elevate them by 12 months finish.

In the meantime, fastened charges have fallen simply barely greater than 100 foundation factors, with five-year phrases lower than that.

Bond yields have been pushed greater just lately by the central financial institution’s determination to maintain charges on maintain and financial information beating expectations. They will also be influenced by inflation, public deficits and worldwide monetary circumstances.

As a result of fastened charges are dictated by market circumstances delays might result in greater somewhat than decrease charges, stated Zlatkin. And even a small enhance in a charge can add as much as greater month-to-month funds, particularly for owners with bigger mortgages.

One shocking development in Canada has been the decline in recognition of the five-year time period, a conventional desire, stated Hendrix Vachon, Desjardins Group principal economist, in a current report.

Earlier than the pandemic, about 30 per cent of recent financing was on a five-year or extra time period, however between 2022 and 2025 that share dropped to fifteen per cent, in response to information from the Financial institution of Canada.

The most well-liked mortgages now are fastened charge with phrases between three and 5 years, accounting for almost 40 per cent of mortgages, he stated.

Zlatkin stated selecting a shorter time period will help debtors safe at this time’s charges whereas leaving room to regulate if circumstances change.

Homebuyers must also take heed. Within the present purchaser’s market, negotiating a greater value will help offset mortgage charges, however timing nonetheless issues.

“Householders who worth predictable funds shouldn’t be ready for an ideal second,” she stated. “On this surroundings, ready can imply paying extra whereas gaining little or no in return.”

Enroll right here to get Posthaste delivered straight to your inbox.

At the moment’s chart from

Royal Financial institution of Canada

provides us an image of simply how unhealthy Toronto’s rental market has grow to be. Pre-construction gross sales in 2025 have been down 90 per cent from the common over the 9 years earlier than 2024, stated RBC.

“The Higher Toronto Space’s new condominium improvement sector has entered a deep freeze with pre-construction gross sales plummeting to ranges not seen for the reason that international monetary disaster,” wrote Robert Hogue, RBC assistant chief economist, in a report in September.

This spells bother for housing development, stated the financial institution. It expects housing begins to fall greater than 10 per cent nationally in 2026 and much more in 2027, regardless of authorities efforts to bolster the nation’s housing provide.

- RBC Capital Markets holds Canadian financial institution CEO convention in Toronto

- Vancouver dwelling gross sales

- How Edward Rogers and Tony Staffieri gained 2025 and what they’ve deliberate for an encore

- Three under-the-radar dangers Canadian buyers ought to concentrate on this 12 months

- Why Caisse CEO Charles Emond thinks Canada is near getting the infrastructure formulation proper

Ought to Margaret, 62, purchase a rental or beef up her investments together with her $275,000 inheritance? Discover out why FP Solutions thinks on this case renting is probably not a foul alternative.

Learn extra

![]()

Considering vitality? The subscriber-only FP West: Vitality Insider e-newsletter brings you unique reporting and in-depth evaluation on one of many nation’s most essential sectors.

Enroll right here.

McLister on mortgages

Wish to be taught extra about mortgages? Mortgage strategist Robert McLister’s

Monetary Publish column

will help navigate the advanced sector, from the newest tendencies to financing alternatives you gained’t wish to miss. Plus verify his

mortgage charge web page

for Canada’s lowest nationwide mortgage charges, up to date every day.

Monetary Publish on YouTube

Go to the Monetary Publish’s

YouTube channel

for interviews with Canada’s main consultants in enterprise, economics, housing, the vitality sector and extra.

At the moment’s Posthaste was written by Pamela Heaven with further reporting from Monetary Publish workers, The Canadian Press and Bloomberg.

Have a narrative concept, pitch, embargoed report, or a suggestion for this article? Electronic mail us at

.

Bookmark our web site and help our journalism: Don’t miss the enterprise information that you must know — add financialpost.com to your bookmarks and join our newsletters right here

![]()

Mortgage debtors

who’ve been holding out for decrease

rates of interest

at the moment are discovering they’ve run out of time, say business professionals.

Fastened-rate mortgages, that are influenced by market circumstances and authorities bond yields, have been drifting greater, rising from a spread of mid-3 per cent this fall to low 4 per cent now.

“Over the previous few months, I’ve seen purchasers flip down fixed-rate renewal affords round 3.7 per cent as a result of they have been satisfied charges would preserve falling,” stated Leah Zlatkin, a mortgage dealer and

LowestRates.ca

knowledgeable.

“Now those self same debtors are coming again and discovering that the most effective out there charges begin with a 4. That delay is already leading to greater month-to-month funds.”

By the top of 2026, greater than a 3rd of Canadian owners will renew their mortgages, lots of them at greater charges from the lows of the pandemic.

Over the previous 12 months, variable charges have dropped greater than fastened, from 7 per cent in June 2024 to barely under 4 per cent because the

Financial institution of Canada

minimize its benchmark charge.

Nevertheless, additional reduction on this entrance now seems to be unlikely with the central financial institution anticipated to maintain charges regular this 12 months or, as some consider, elevate them by 12 months finish.

In the meantime, fastened charges have fallen simply barely greater than 100 foundation factors, with five-year phrases lower than that.

Bond yields have been pushed greater just lately by the central financial institution’s determination to maintain charges on maintain and financial information beating expectations. They will also be influenced by inflation, public deficits and worldwide monetary circumstances.

As a result of fastened charges are dictated by market circumstances delays might result in greater somewhat than decrease charges, stated Zlatkin. And even a small enhance in a charge can add as much as greater month-to-month funds, particularly for owners with bigger mortgages.

One shocking development in Canada has been the decline in recognition of the five-year time period, a conventional desire, stated Hendrix Vachon, Desjardins Group principal economist, in a current report.

Earlier than the pandemic, about 30 per cent of recent financing was on a five-year or extra time period, however between 2022 and 2025 that share dropped to fifteen per cent, in response to information from the Financial institution of Canada.

The most well-liked mortgages now are fastened charge with phrases between three and 5 years, accounting for almost 40 per cent of mortgages, he stated.

Zlatkin stated selecting a shorter time period will help debtors safe at this time’s charges whereas leaving room to regulate if circumstances change.

Homebuyers must also take heed. Within the present purchaser’s market, negotiating a greater value will help offset mortgage charges, however timing nonetheless issues.

“Householders who worth predictable funds shouldn’t be ready for an ideal second,” she stated. “On this surroundings, ready can imply paying extra whereas gaining little or no in return.”

Enroll right here to get Posthaste delivered straight to your inbox.

At the moment’s chart from

Royal Financial institution of Canada

provides us an image of simply how unhealthy Toronto’s rental market has grow to be. Pre-construction gross sales in 2025 have been down 90 per cent from the common over the 9 years earlier than 2024, stated RBC.

“The Higher Toronto Space’s new condominium improvement sector has entered a deep freeze with pre-construction gross sales plummeting to ranges not seen for the reason that international monetary disaster,” wrote Robert Hogue, RBC assistant chief economist, in a report in September.

This spells bother for housing development, stated the financial institution. It expects housing begins to fall greater than 10 per cent nationally in 2026 and much more in 2027, regardless of authorities efforts to bolster the nation’s housing provide.

- RBC Capital Markets holds Canadian financial institution CEO convention in Toronto

- Vancouver dwelling gross sales

- How Edward Rogers and Tony Staffieri gained 2025 and what they’ve deliberate for an encore

- Three under-the-radar dangers Canadian buyers ought to concentrate on this 12 months

- Why Caisse CEO Charles Emond thinks Canada is near getting the infrastructure formulation proper

Ought to Margaret, 62, purchase a rental or beef up her investments together with her $275,000 inheritance? Discover out why FP Solutions thinks on this case renting is probably not a foul alternative.

Learn extra

![]()

Considering vitality? The subscriber-only FP West: Vitality Insider e-newsletter brings you unique reporting and in-depth evaluation on one of many nation’s most essential sectors.

Enroll right here.

McLister on mortgages

Wish to be taught extra about mortgages? Mortgage strategist Robert McLister’s

Monetary Publish column

will help navigate the advanced sector, from the newest tendencies to financing alternatives you gained’t wish to miss. Plus verify his

mortgage charge web page

for Canada’s lowest nationwide mortgage charges, up to date every day.

Monetary Publish on YouTube

Go to the Monetary Publish’s

YouTube channel

for interviews with Canada’s main consultants in enterprise, economics, housing, the vitality sector and extra.

At the moment’s Posthaste was written by Pamela Heaven with further reporting from Monetary Publish workers, The Canadian Press and Bloomberg.

Have a narrative concept, pitch, embargoed report, or a suggestion for this article? Electronic mail us at

.

Bookmark our web site and help our journalism: Don’t miss the enterprise information that you must know — add financialpost.com to your bookmarks and join our newsletters right here

{kind=link}