Up to date on July ninth, 2026 by Josh Arnold

We imagine that long-term traders ought to give attention to the highest-quality dividend-growth shares. These are corporations with lengthy histories of elevating their dividends, and sturdy aggressive benefits to gasoline continued dividend progress.

Subsequently, we are likely to steer traders towards the Dividend Kings, a gaggle of simply 58 shares which have maintained at the least 50 years of consecutive dividend will increase.

It’s also possible to obtain an Excel spreadsheet with the complete listing of all 58 Dividend Kings (plus vital metrics akin to price-to-earnings ratios and dividend yields) by clicking on the hyperlink under:

We assessment every of the Dividend Kings yearly. The next inventory to be reviewed on this 12 months’s version is AbbVie (ABBV).

There are questions relating to AbbVie’s future progress, as its flagship drug, Humira, is going through patent expiration in numerous levels throughout the globe. Nonetheless, the corporate has a plan to proceed rising within the years forward. This text will give attention to AbbVie’s prospects as a core dividend holding.

Enterprise Overview

AbbVie is a worldwide pharmaceutical large. It started buying and selling as an unbiased firm in 2013, having been spun off from Abbott Laboratories (ABT). Because the spin-off, AbbVie has generated robust progress. Earnings-per-share have elevated on a median annual tempo of about 12.5% from 2016 to 2025.

Right this moment, AbbVie focuses on a single important enterprise phase: prescribed drugs. It focuses on a number of key therapy areas, together with immunology, hematologic oncology, neuroscience, and others.

Because the spin-off from Abbott, AbbVie has skilled glorious progress, primarily pushed by Humira, a multi-purpose drug. The problem for AbbVie is that Humira is now going through biosimilar competitors after it has misplaced patent exclusivity.

Even so, AbbVie stays a large within the healthcare sector, with an in depth and diversified product portfolio.

Earnings got here to $2.65 per share in the course of the quarter, which was increased by 8% in comparison with the year-ago interval. That did, nevertheless, miss estimates by two cents. The achieve in revenue was pushed by increased income and a few revenue margin enlargement. Steerage was up to date to $14.08 to $14.28 per share in earnings, and if achieved, would characterize a brand new file for the corporate. We’ve set our estimate proper within the center at $14.18.

Development Prospects

The numerous danger for world pharmaceutical producers is the lack of patent safety. When a specific drug loses patent, the market is often flooded with competitors, particularly for the world’s top-selling merchandise.

AbbVie’s greatest danger is the upcoming competitors to its flagship drug, Humira. This multi-purpose drug is used to deal with a wide range of situations, together with rheumatoid arthritis, plaque psoriasis, Crohn’s illness, ulcerative colitis, and extra.

Humira as soon as generated over half of AbbVie’s annual gross sales. Lack of patent exclusivity is a big overhang; in consequence, AbbVie’s whole gross sales declined in 2023. Regardless of this, income progress returned in 2025 and is anticipated to develop for the foreseeable future.

Thankfully, the corporate ready for the lack of patent exclusivity on Humira by investing closely in new merchandise and acquisitions to spice up its progress. For instance, Rinvoq and Skyrizi are two key merchandise that characterize long-term progress catalysts.

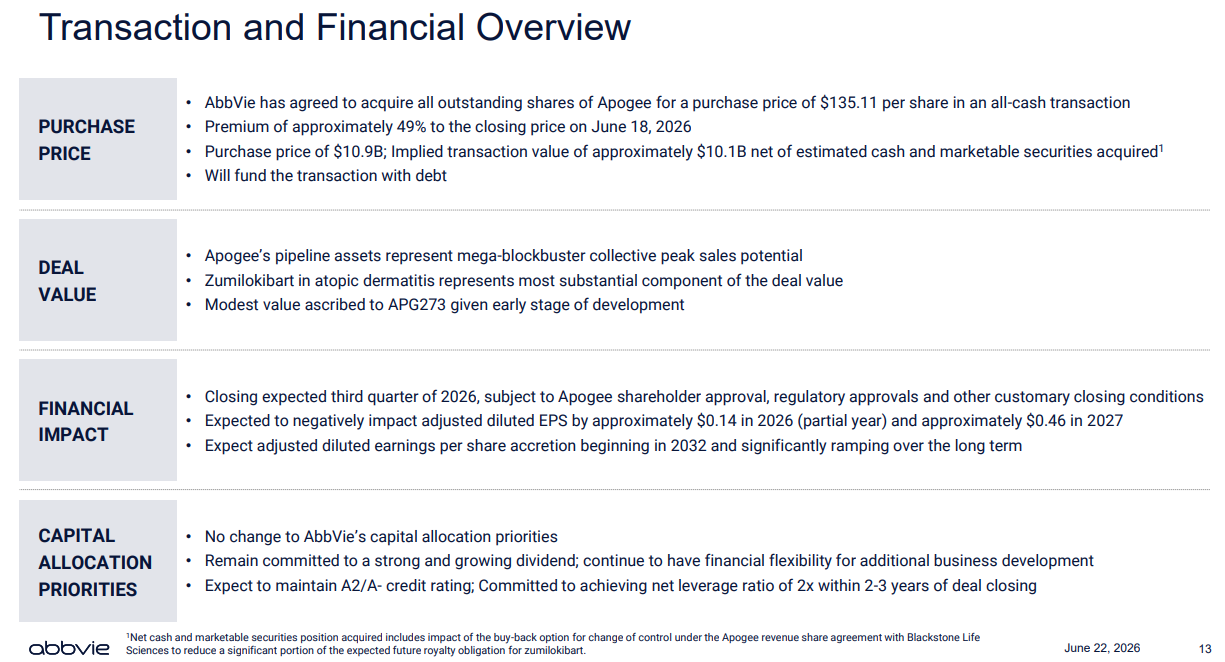

As well as, it pretty repeatedly makes acquisitions, akin to its very latest announcement of the acquisition of Apogee Therapeutics, Inc. (APGE) for about $11 billion.

Supply: Investor presentation

AbbVie additionally accomplished the $63 billion acquisition of Allergan just a few years in the past, which was an unlimited buy. Allergan’s flagship product is Botox, which diversifies AbbVie’s portfolio by exposing it to the worldwide aesthetics market.

We count on AbbVie to realize 6% EPS progress over the subsequent 5 years. We imagine the expansion outlook will enhance as soon as the Humira overhang is resolved, however we not the uncertainty surrounding income progress with the Humira expiration is basically being resolved, and the outlook is brighter than it’s been in recent times.

Aggressive Benefits & Recession Efficiency

Probably the most vital aggressive benefit for AbbVie and any pharmaceutical firm is its patent portfolio. Pharmaceutical giants should make investments closely in growing new medicine and therapies when considered one of their blockbusters loses patent safety.

AbbVie has over 60 scientific packages. It has a number of progress alternatives to exchange Humira, notably within the therapeutic areas of immunology, hematology, and neuroscience. The results of its vital funding in R&D is a well-stocked pipeline. That is complimentary to its focused acquisition technique.

AbbVie was not a standalone firm over the past monetary disaster, so it doesn’t have a recession monitor file. Nonetheless, since sick folks require therapy whatever the financial system’s energy, it’s extremely seemingly that AbbVie would proceed to carry out properly throughout a recession.

AbbVie’s earnings are more likely to decline considerably throughout a recession, however the dividend is anticipated to stay safe. AbbVie has a projected dividend payout ratio of ~49% for 2026.

Valuation & Anticipated Returns

AbbVie is anticipated to generate adjusted EPS of $14.18 for 2026 on the midpoint of steerage. At this EPS stage, the inventory presently has a price-to-earnings ratio of 17.8.

Our truthful worth estimate for AbbVie is a price-to-earnings ratio of 13, indicating that the inventory is presently materially overvalued. A declining P/E a number of might cut back shareholder returns by roughly 5% per 12 months over the subsequent 5 years.

Moreover, we anticipate annual earnings progress of 6% by 2030.

Lastly, the inventory has a present dividend yield of two.7%. Given these inputs, we count on annual returns of two% or 3% per 12 months over the subsequent 5 years, making AbbVie inventory a maintain regardless of its exemplary dividend historical past.

Remaining Ideas

AbbVie is a high-quality enterprise, boasting a powerful pharmaceutical pipeline and vital progress potential. It is usually a shareholder-friendly firm that returns extra money stream to traders by inventory buybacks and dividends.

AbbVie faces a big problem in changing misplaced Humira gross sales, because it competes with different corporations within the U.S. and Europe. For this reason now we have pretty low assumptions for the corporate’s future EPS progress and truthful worth P/E a number of.

Nonetheless, the corporate has constructed an in depth portfolio of recent merchandise that ought to assist keep its progress, in addition to acquisitions. Nonetheless, the anticipated returns make the inventory a maintain.

Further Studying

The next databases of shares include shares with very lengthy dividend or company histories, ripe for choice for dividend progress traders.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

")

")

{kind=link}