Up to date on February sixth, 2026 by Nathan Parsh

PPG Industries (PPG) is among the largest paint firms on this planet. Additionally it is probably the most dependable dividend shares out there—PPG has paid dividends each quarter since 1899.

Furthermore, the corporate has elevated its dividend annually for the final 54 years, which qualifies it for the unique Dividend Aristocrats checklist.

This can be a group of 69 shares within the S&P 500 Index which have had a minimum of 25 consecutive years of dividend progress.

We contemplate the Dividend Aristocrats to be among the many elite dividend-paying firms. With this in thoughts, we created a full checklist of all 69 Dividend Aristocrats.

You’ll be able to obtain your entire Dividend Aristocrats checklist, with necessary monetary metrics like dividend yields and P/E ratios, by clicking on the hyperlink beneath:

Disclaimer: Certain Dividend shouldn’t be affiliated with S&P World in any approach. S&P World owns and maintains The Dividend Aristocrats Index. The data on this article and downloadable spreadsheet is predicated on Certain Dividend’s personal assessment, abstract, and evaluation of the S&P 500 Dividend Aristocrats ETF (NOBL) and different sources, and is supposed to assist particular person traders higher perceive this ETF and the index upon which it’s based mostly. Not one of the data on this article or spreadsheet is official knowledge from S&P World. Seek the advice of S&P World for official data.

The inventory can also be on the unique checklist of Dividend Kings.

PPG’s exceptional dividend consistency offers it broad enchantment to the extra conservative members of the dividend progress investing group.

Certainly, the corporate’s sturdy enterprise mannequin ensures a really secure dividend fee and room for regular dividend will increase annually. That is nonetheless very a lot the case right now.

This text will analyze PPG’s funding prospects intimately and decide whether or not the corporate deserves a purchase suggestion at present costs.

Enterprise Overview

PPG Industries was based in 1883 as a glass producer and distributor. The corporate’s identify, Pittsburgh Plate Glass, refers to its authentic operations.

Over time, PPG has made exceptional strides to turn into a frontrunner within the paints and coatings trade.

With annual revenues of about $16 billion, PPG’s solely rivals of comparable dimension are fellow Dividend Aristocrat Sherwin-Williams (SHW) and Dutch paint firm Akzo Nobel (AKZOY).

Because of its worldwide working presence and concentrate on expertise and innovation, PPG Industries has grown to such a formidable dimension.

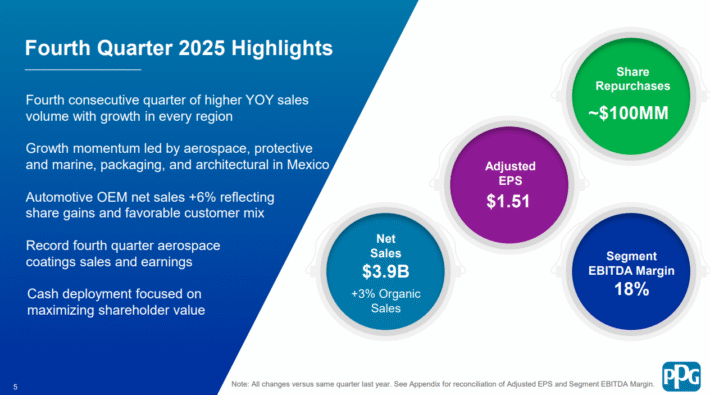

On January twenty seventh, 2026, PPG Industries reported fourth-quarter and full yr outcomes for the interval ending December thirty first, 2025.

Supply: Investor Presentation

For the quarter, income grew 4.8% to $3.91 billion, which was $140 million greater than anticipated. Adjusted earnings-per-share of $1.51 in contrast unfavorably to $1.61 within the prior yr and was $0.07 lower than anticipated.

For the yr, income from persevering with improved 0.6% to $15.9 billion whereas adjusted earnings-per-share of $7.58 was down from $7.87 in 2025.

Fourth-quarter natural income progress was greater by 3% whereas full yr outcomes elevated 2%. World Architectural Coatings’ income, previously a part of Efficiency Coatings, grew 8% to $951 million for the quarter. Increased costs added 2% whereas overseas forex translation was a 9% tailwind to outcomes. Quantity was unchanged. Latin America and Asia Pacific have been as soon as once more sturdy in the course of the interval.

Efficiency Coatings was up 5% to $1.32 billion as a 4% improve in costs and a small contribution from forex alternate offset a 1% drop in quantity. Aerospace posted document outcomes and the backlog elevated $315 million.

The Industrial Coatings section was greater by 3% to $1.64 billion as quantity positive factors have been offset by weaker costs and divestitures. Automotive OEMs produced one other quarter of progress as this section outpaced the worldwide trade.

PPG Industries repurchased ~$100 million of shares throughout This fall and and retired ~$790 million value of inventory throughout 2025. The corporate has $2.0 billion, or ~7.1% of its present market capitalization, remaining on its share repurchase authorization.

For 2026, the corporate expects natural gross sales to be in a variety of flat to up a low single-digit share. Adjusted earnings-per-share in a variety of $7.70 to $8.10. On the midpoint, this may symbolize a 4.2% enchancment from 2025.

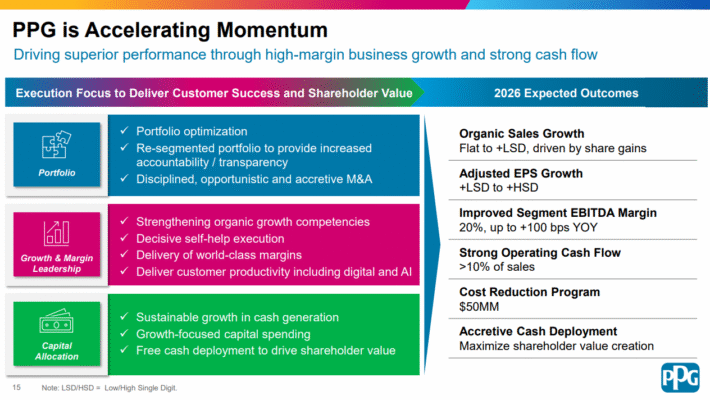

Progress Prospects

An organization’s capability to extend revenues and earnings is essentially a perform of its capital allocation.

In recent times, PPG has spent billions of {dollars} shopping for its subsequent era of progress. It tries to take care of a considerably balanced capital allocation technique, however it’s also not afraid to spend large on acquisitions when alternatives current themselves.

PPG has spent far more of its deployed money on share repurchases than its rivals, which has been a serious supply of earnings-per-share progress over time.

Acquisitions have been a key progress driver for PPG for a few years. That progress has come at a price, particularly a rise within the firm’s debt.

PPG is now just about solely a coatings enterprise. In recent times, the corporate has reworked away from legacy companies like glass and chemical compounds, leaving it with a portfolio of coatings merchandise that collectively generate almost $16 billion in annual income. These companies have largely seen enhancements in margins lately.

Its monitor document means that its underlying enterprise is more likely to proceed rising at a passable charge for the foreseeable future. Up to now decade, the corporate has grown its earnings-per-share at a mean charge of just below 10%, however this progress charge deaccelerates to three.1% when taking a look at simply the final 5 years.

Whereas the declining progress charge is clear and regarding, we consider that the corporate has the power to develop at a excessive single-digit charge given its sturdy fundamentals.

Supply: Investor Presentation

We consider traders can fairly anticipate 7% adjusted earnings-per-share progress from PPG Industries by full financial cycles.

Nevertheless, PPG’s efficiency is more likely to undergo during times of financial recession. The excellent news is that we might probably see such an occasion as a shopping for alternative for this high-quality enterprise.

Aggressive Benefits & Recession Efficiency

PPG enjoys a number of aggressive benefits. It operates within the paints and coatings trade, which is economically enticing for a number of causes. First, these merchandise have excessive revenue margins for producers.

Additionally they have low capital funding, which ends up in vital money movement. As mentioned above, PPG has used this vital money movement over time.

Given all this, it is smart that solely two coatings firms (Sherwin-Williams and PPG Industries) are on the Dividend Aristocrats checklist.

That stated, the paint and coatings trade shouldn’t be recession-resistant as a result of it depends upon wholesome housing and development markets. This affect might be seen in PPG’s efficiency in the course of the 2007-2009 monetary disaster:

- 2007 adjusted earnings-per-share: $2.52

- 2008 adjusted earnings-per-share: $1.63 (35% decline)

- 2009 adjusted earnings-per-share: $1.02 (37% decline)

- 2010 adjusted earnings-per-share: $2.32 (127% improve)

PPG’s adjusted earnings-per-share fell by greater than 50% over the last main recession and took two years to get better.

As PPG’s 2020 outcomes confirmed, the decline in new development is the dominant issue throughout a recession. The 2020 recession was no completely different, as PPG confronted manufacturing unit shutdowns and severely diminished client demand, though that proved to be transitory.

Whereas this Dividend Aristocrat’s long-term prospects stay vivid, traders must be keen to simply accept volatility in a recession.

Valuation & Anticipated Whole Returns

We’re forecasting earnings-per-share of $7.90 for the fiscal yr of 2026, placing the price-to-earnings ratio at 15.7. That is beneath our honest worth estimate of 19 occasions earnings, that means PPG is undervalued right now.

As such, we anticipate complete returns from valuation enlargement to extend by 3.9% yearly over the subsequent 5 years.

In complete, we mission that PPG will return 13.0% yearly by 2031, stemming from 7% earnings progress and the beginning yield of two.3%, together with a 3.9% annualized return from an increasing P/E a number of.

Last Ideas

PPG Industries has most of the traits of a really high-quality enterprise. Its confirmed enterprise mannequin has allowed the corporate to climate any recession.

It additionally has a big worldwide presence and a number of catalysts for future progress. Lastly, it has elevated its dividend for greater than 50 years.

PPG’s dividend outlook is exemplary and we see many extra years of dividend will increase on the horizon. With anticipated annual returns of 13%, we charge PPG inventory a purchase.

In case you are focused on discovering high-quality dividend progress shares appropriate for long-term funding, the next Certain Dividend databases can be helpful:

The main home inventory market indices are one other stable useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

: A Bull Case Theory")

{kind=link}