Up to date on April seventeenth, 2025 by Nathan Parsh

Traders in search of excessive yields could contemplate buying shares of Enterprise Improvement Corporations, also referred to as BDCs. These shares steadily have a better dividend yield than the broader inventory market common.

Some BDCs even pay month-to-month dividends.

You may obtain our full Excel spreadsheet of all month-to-month dividend shares (together with metrics that matter, like dividend yield and payout ratio) by clicking on the hyperlink beneath:

Oxford Sq. Capital Company (OXSQ) is a Enterprise Improvement Firm (BDC) that pays a month-to-month dividend. Oxford Sq. can be a extremely yielding inventory, with a yield of practically 17% based mostly on anticipated dividends for fiscal 2025. That is 12 occasions the common yield of the S&P 500.

Nevertheless, buyers ought to all the time remember that the sustainability of a dividend is simply as essential, if no more so, than the yield itself.

BDCs usually present excessive ranges of earnings, however many (together with Oxford Sq.) have bother sustaining their dividends, notably throughout recessions. This text will look at the corporate’s enterprise, development prospects, and consider the security of the dividend.

Enterprise Overview

Oxford Sq. Capital Corp. is a Enterprise Improvement Firm (BDC) specializing in financing early- and middle-stage companies by means of loans and Collateralized Mortgage Obligations (CLOs). You may see our full BDC record right here.

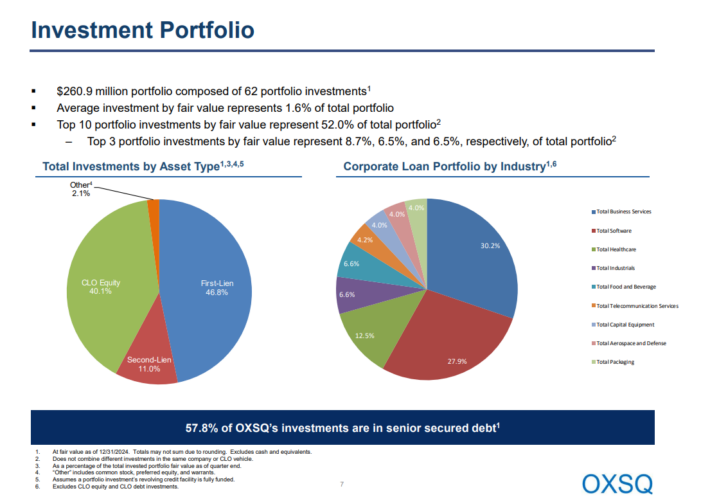

The corporate holds a well-diversified portfolio of First–Lien, Second–Lien, and CLO fairness property unfold throughout seven industries, with the best publicity in enterprise companies and software program, at 30.2% and 27.9%, respectively.

Supply: Investor presentation

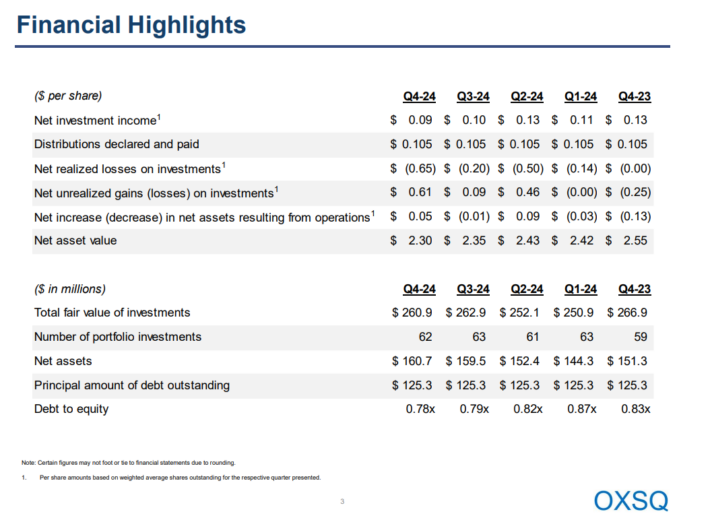

On February 28, 2025, Oxford Sq. introduced its This fall and 2024 outcomes for the interval ended December 31, 2024.

Supply: Investor presentation

The corporate reported complete funding earnings of $42.7 million for the 12 months, a lower of $9.1 million from the earlier 12 months. This decline was primarily resulting from a discount in curiosity earnings from debt investments.

The weighted common yield on debt investments improved to fifteen.8% from 13.3% within the earlier 12 months. The money distribution yield on money income-producing CLO fairness investments rose barely to 16.2% from 15.3% on a sequential foundation. The efficient yield on CLO fairness investments was 8.8%, down marginally from 9.6% in Q3 2024.

Complete bills had been $16.2 million for the 12 months, down considerably from $24.5 million within the prior 12 months as a result of absence of incentive charges.

Consequently, internet funding earnings (NII) totaled $26.4 million, or $0.42 per share, in comparison with $27.4 million, or $0.48 per share, within the earlier 12 months. The corporate’s internet asset worth (NAV) per share of $2.30 was down from $2.55 a 12 months in the past. Primarily based on its present portfolio, Oxford Sq. tasks to have a full-year 2025 funding earnings per share (IIS) of $0.42.

Development Prospects

The corporate’s funding earnings per share had been declining at an alarming fee, as financing grew to become cheaper, stopping Oxford Sq. from refinancing at its earlierly larger charges. Moreover, the corporate has traditionally over-distributed dividends to shareholders, thereby eroding its NAV and future earnings technology resulting from lowered asset holdings.

Contemplating that the Fed has not lower rates of interest as a result of present financial uncertainty, we anticipate Oxford Sq. to generate secure funding earnings per share within the close to time period.

The 2020 dividend lower ought to allow Oxford Sq. to retain some money, hopefully permitting it to begin regrowing its NAV. With charges unlikely to proceed moving any decrease for the second, earnings technology ought to stabilize.

With funding throughout a large breadth of various industries, Oxford Sq. has a fairly balanced portfolio. The corporate’s prime three industries do make up a lot of the portfolio, however they’re in numerous areas of the economic system. This gives some safety within the occasion of a downturn in a single trade.

Nevertheless, if charges decline over time, the corporate’s receivables might be additional pressured, worsening its monetary efficiency yearly. Total, we consider that the corporate’s future investment earnings technology carries substantial dangers, whereas a possible recession and an antagonistic financial setting may severely harm its curiosity earnings.

Dividend Evaluation

Oxford Sq. solely just lately started paying a month-to-month dividend, with the primary being distributed in April 2019. Complete dividends paid over the previous few years are listed beneath:

- 2015 dividends: $1.14

- 2016 dividends: $1.16 (1.8% improve)

- 2017 dividends: $0.80 (31% decline)

- 2018 dividends: $0.80 (no improve)

- 2019 dividends: $0.80 (no improve)

- 2020 dividends: $0.6120 (23.5% decline)

- 2021 dividends: $0.42 (31.4% decline)

- 2022 dividends: $0.42 (Flat)

- 2023 dividends: $0.54(28.5% improve)

- 2024 dividends: $0.42 (22% decline)

Shareholders acquired a small improve in 2016, adopted by three giant dividend reductions since 2017. This inconsistency in dividend payout is as a result of firm’s unstable monetary efficiency. Final 12 months’s dividend complete was negatively impacted by the absence of a $0.12 per share particular dividend that occurred in 2023. The month-to-month cost has remained the identical because the 2020 lower.

Oxford Sq. at the moment pays a month-to-month dividend of $0.035 per share, equaling an annualized payout of $0.42 per share.

Primarily based on a full-year payout of $0.42 per share, Oxford Sq. inventory yields 16.9%. Though the dividend cuts lately have been substantial, the dividend yield stays remarkably excessive. That stated, buyers shouldn’t focus solely on yield; dividend security is a vital consideration for earnings buyers, and on this regard, Oxford Sq. leaves quite a bit to be desired.

Primarily based on our expectation of a full-year funding earnings per share of $0.42 for 2025, the corporate is projected to take care of a 100% dividend payout ratio for 2025. Nevertheless, if funding earnings declines from present ranges, one other dividend lower may end result.

Closing Ideas

Oxford Sq. boasts a strong enterprise mannequin, characterised by diversification throughout numerous funding property and industries. The corporate has additionally taken steps to construct up its much less dangerous asset place whereas reducing its reliance on riskier CLOs.

That stated, Positive Dividend recommends that risk-averse buyers keep away from Oxford Sq.. We consider that the dividend doesn’t provide sufficient security. The corporate distributes basically all of its funding earnings, leaving little room for maneuver. Any decline in funding earnings may result in additional dividend cuts, making Oxford Sq. a much less enticing funding possibility for buyers in search of secure and safe sources of earnings.

Don’t miss the assets beneath for extra month-to-month dividend inventory investing analysis.

And see the assets beneath for extra compelling funding concepts for dividend development shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}