Let’s take a look at some photos of the growing danger state of affairs within the US inventory market, in gentle of Inauguration day upcoming on January 20, 2025, when the brand new president can be sworn in and his “Make America Nice Once more” jingle reconstituted. This group of indicators is much from exhaustive, as we use a number of different indicators and instruments, lots of which additionally presently forecast a coming section when danger is to be realized, relatively than simply implied, as it’s now.

That in itself – the likelihood that a big proportion of market individuals consider that the “businessman” president can be good for equities – is a big opposite indicator by itself, with the election hype coming after a 12 months when the earlier administration did all it might to maintain the markets propped (efficiently, and but they have been nonetheless ousted). The company tax slicing, deregulating new(ish) president might certainly become good for equities, however we’re speaking market forces within the right here and now and the prospect of an oncoming bear section, versus the 4 12 months presidential time period upcoming.

I don’t personally handle the markets from the long-term “shares all the time return up once more” perspective that’s so adhered to by a overwhelming majority. I need to miss the market liquidations, draw-downs and crashes, thanks very a lot. I need to catch the shopping for alternatives, a we did in Q1-Q2, 2020. As we did in This fall, 2008. Certainly, NFTRH was launched on September twenty eighth of that 12 months, partly as a result of I noticed the epic purchase alternatives shaping up on the time and thought ‘it’s now or by no means’.

Whereas not an achieved quick vendor by any means, I’d wish to attempt to patiently set as much as capitalize on coming bearish occasions as effectively. However that may be a lesser precedence when money and high quality equivalents ought to handle danger simply wonderful – and pay out revenue alongside the best way.

This survey from AAII (Ma & Pa, AKA particular person buyers) members was taken after the election of 1 Donald J. Trump. 40% of members see the election consequence as optimistic for shares and 63% see it as impartial or higher. When you think about that half the nation’s inhabitants voted in opposition to Trump, the outcomes are clear; it’s a bearish opposite indicator.

With the wanting upward at our working goal of 6180, a doubtlessly closing suck-in of the (dumb cash) FOMOs is in progress. The each day RSI divergence helps the view of a coming high of some form.

Whereas there will be lengthy phases when opposite indications are in place however shares proceed to rise or stay aloft, public sentiment will all the time be over-bullish at essential market tops. The Public Optimism/Pessimism unfold is presently over-bullish and is an intact “situation” for a market high, not a timing software for a high.

Right here is an fascinating historic indicator, the BMPM or Bear Market Chance Mannequin. This indicator is cooked up by Goldman Sachs utilizing 5 basic inputs: the U.S. Unemployment Price, ISM Manufacturing Index, Yield Curve, Inflation Price, and P/E Ratio. Regardless of the inputs, the indicator’s forecasting file is great, though its timing file, like many inner and sentiment indicators, shouldn’t be good. So it’s one other indicator that’s an intact situation for a high. Huge time.

Most notably now, the final two main promote alternatives, 2006-2008 and 2019-2020 got here after the indicator had been slipping for prolonged intervals (orange arrows). My competition is that the 2022 correction has been inappropriately labeled a bear market by a majority of individuals and media. In 2022 the SPX development (larger highs/lows) remained intact to its bull market that started in 2009. It was a wholesome correction, not a bear market. All of it occurred inside a type of prolonged slips within the BMPM and that slippage remains to be in play. Threat may be very excessive by this indicator.

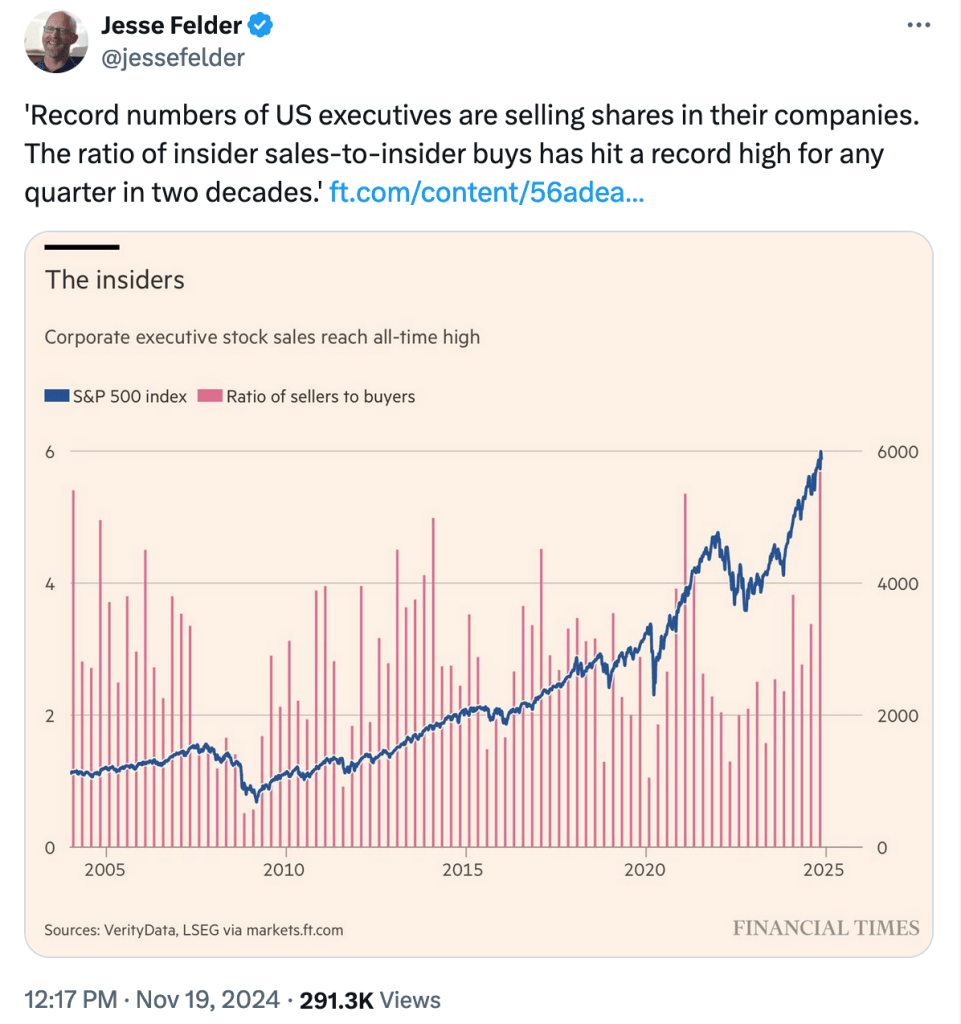

Jesse Felder had a very good presentation of a few danger indicators, the web promoting of company insiders and the market’s nosebleed valuations, on November 22. Right here is the graph displaying one other topping “situation” (versus a timer) presently in place.

From the vantage level of the Junk bond market we discover buyers’ urge for food for the riskiest bonds (and their larger payouts) relative to high quality bonds to be gluttonous, to an epic diploma. Excessive investor complacency (and greed) like this can be in place on the subsequent market high.

From the vantage level of market volatility, you may insert the identical conclusion as instantly above, with the added aspect of a still-intact divergence by the to the northerly touring , going its approach, seemingly with out a care on the planet. This divergence provides extra warning to the excessive danger sign (and topping “situation”, not timer) of a particularly depressed VIX, which is able to all the time be in that state at essential market tops.

There are a lot of extra market indicators and internals, from the Semiconductor > Tech > Broad (SPX) management chain, to yield curves, to the still-intact divergence of the 2yr Treasury yield to the (Fed proxy) 3 month T-bill yield, to the combo of the US greenback and the Gold/Silver ratio, and so many different indicators guiding the best way ahead and offering us with a easy, manageable path as they’ve all 12 months.

I’d wish to make a closing observe. When presenting bearish evaluation just like the above, it is very important disclaim private standing. As of the writing of this text, I’m not (but) speaking my e book as a result of the one present quick place in my e book is a hedge on the gold mining sector. At the moment, I’m in a gradual strategy of promoting and internet revenue taking, very like the company insiders are presently doing as they money out whereas dumb cash FOMOs and drives the market’s closing MOMO section. I’m additionally build up defensive positions relative to risk-on positions. Money is the last word protection, sure sectors are defensive and short-term Treasury bonds are defensive. All of these are actively favored proper now.

{kind=link}