Skip to content material

![]()

The US economic system is experiencing quite a lot of shocks popping out of fast and big alterations in authorities on the federal degree, sweeping modifications to commerce and tariff coverage, and dislocations in beforehand allotted federal {dollars} together with renewing tax cuts to the wealthiest People. Within the present atmosphere, client and enterprise uncertainty are elevated. Anticipation of a recession is growing. Are recession flags waving? Not fairly but, however the wind appears to be choosing up.

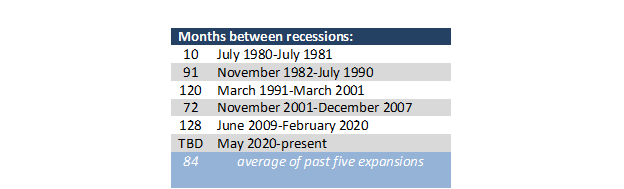

Chair Jerome Powell has mentioned that the Federal Reserve doesn’t have a recession in its forecast, however that the dangers for one are higher. The US economic system has skilled a protracted interval of progress after the trough of the Nice Recession (December 2007 to June 2009) with uninterrupted enlargement since then aside from the report temporary recession related to the Covid-19 shutdowns (February-April 2020).

Former Fed Chair Janet Yellen has famously mentioned that expansions don’t die of previous age in reference to the lengthy enlargement after the Nice Recession and earlier than the pandemic. Former Fed Chair Ben Bernanke added the corollary that they’re murdered. The purpose is that the size of an enlargement isn’t essentially an indication of its imminent demise, somewhat that expansions finish because of exogenous occasions that severely have an effect on the economic system’s clean functioning and skill to recuperate from the shock.

The query is that if the insurance policies and actions of the Trump administration goes to carry on a recession. The quick reply is that it’s in all probability too quickly to inform. There are just a few indicators that may pretty reliably wave the warning flag.

The Nationwide Bureau of Financial Analysis (NBER) is the guardian of assigning dates to financial peaks and troughs that demarcate a recessionary interval. The NBER defines a recession as “a big decline in financial exercise unfold throughout the economic system, lasting quite a lot of months, usually seen in actual GDP, actual earnings, employment, industrial manufacturing, and wholesale-retail gross sales.” It may well take them months after a recession has began to make the official name.

Those that watch the economic system intently – markets, central bankers, politicians, and so forth. – can’t watch for the NBER and must act based mostly on present data. They want some framework for early warning of a downturn and depend on just a few guidelines of thumb for calling a recession. These are:

• Two consecutive quarters of unfavourable GDP progress.

• A persistent enhance within the unemployment price of greater than 50 foundation factors from its cyclical low.

• An inverted yield curve.

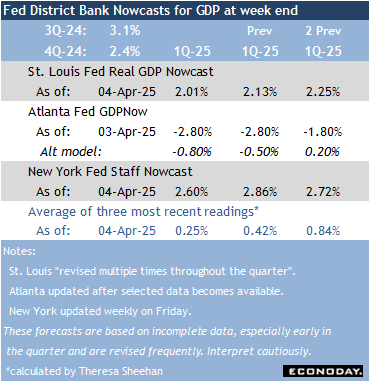

After the wild swings in GDP within the first months of the pandemic in 2020, GDP settled into a virtually unbroken string of quarter with modest-to-moderate enlargement by the fourth quarter 2024. That progress seems to be in jeopardy within the first quarter of 2025. Companies and shoppers front-loaded some spending within the fourth quarter 2024 with the looming risk of upper costs associated to tariffs. Probably the most correct of the three Fed district financial institution GDP Nowcasts factors to a contraction within the first quarter 2025. The Atlanta Fed GDPNow forecasts unfavourable 2.8 % progress within the first quarter. Their mannequin was significantly swayed by the massive exports of nonmonetary gold in January and February. Their various mannequin excluding that also appears for contraction of 0.8 % within the first quarter. Nonetheless, The St. Louis Fed GDP Nowcast is for GDP to rise 2.01 % and the New York Fed Employees Nowcast is for up 2.6 %. The advance estimate for first quarter GDP is ready for launch at 8:30 ET on Wednesday, April 30.

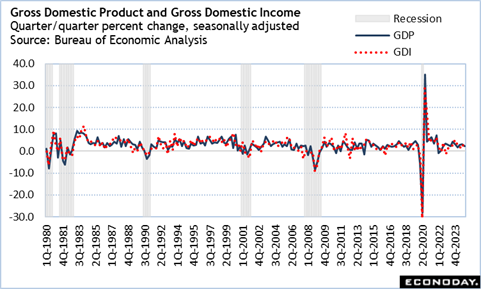

One factor that could be a counter to the recession narrative is the efficiency of gross home earnings (GDI). Word that the NBER doesn’t simply take a look at progress, but additionally earnings. If GDI doesn’t weaken, it might recommend that any dip in GDP progress is overstated.

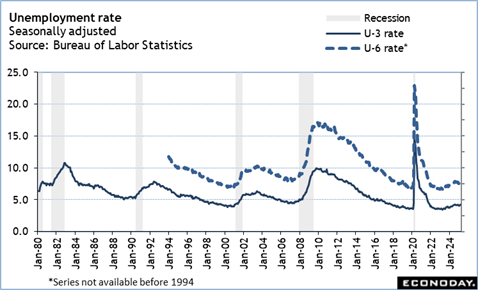

The unemployment price – or U-3, whole unemployed as a % of the civilian labor pressure – is the official unemployment price. Nonetheless, it’s also helpful to observe the U-6 price – whole unemployed, plus all folks marginally connected to the labor pressure, plus whole employed half time for financial causes, as a % of the civilian labor pressure plus all folks marginally connected to the labor pressure – because the broadest measure of unemployment. A weakening job market tends to have an effect on those that are among the many much less employable first.

The unemployment price has plunged from its peak of 14.8 % in April 2020 to three.4 % in April 2023. It slowly and inconsistently labored its method again as much as 4.2 % in July 2024. Since then, it has been in a slender vary of 4.0 % to 4.2 %. It’s too quickly to say it’s vital, however the U-3 price has risen from 4.0 % in January to 4.1 % in February to 4.2 % in March. That is solely 20 of the 50 foundation factors that may represent a louder inflation sign, but when the unemployment price reaches 4.3 % or increased in April it’s a trigger for concern.

Extra instantly regarding is that the U-6 price rose fifty foundation factors in February to eight.0 %, though it backed down a tenth to 7.9 % in March. Nonetheless, February and March are the best readings since 8.2 % in October 2021.

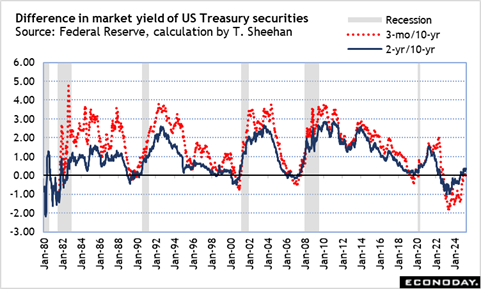

The hole between the 2-year/10-year Treasury yields – which the Fed watches greater than the extra unstable 3-month invoice/10-year notice habits – typically precedes a recession. The newest episode in 2023 was extra concerning the inflation battle at a time of modest-to-moderate enlargement. That has lifted towards the tip of 2024 and into early 2025. Nonetheless, the distinction available in the market yields stays slender with shorter-term securities extra in demand in a time of uncertainty.

There are different indications of a weakening economic system which are price maintaining a tally of.

Inventory market habits isn’t usually thought-about a sign of a recession. Typically a pointy drop is a correction or a response to short-term occasions, not a warning. Nonetheless, it shouldn’t be ignored.

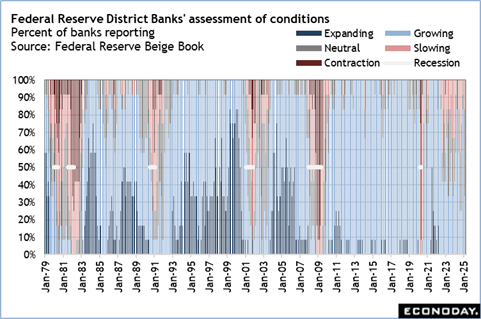

Though the Fed’s Beige Ebook is just not arduous knowledge, the anecdotal proof about financial situations throughout the 12 districts is present and an correct evaluation of enterprise and client exercise. When 7 or fewer districts broadly describe exercise as rising, it’s a sturdy chance {that a} recession is within the works. An exception has been the interval between July 2022 and October 2024 when the economic system was nonetheless recovering from provide chain disruptions and coping with inflation even because the labor provide was tight and demand was excessive. Strong employment saved a recession at bay. The Beige Books launched in December 2024 and January 2025 gave each indication that exercise was on the rise and the economic system was increasing comfortably throughout the districts. Nonetheless, the newest one launched in March mirrored an abrupt deterioration in situations from one hundred pc of districts reporting at the least some progress within the interval between late November and early January to solely 33 % within the interval between early January and late February. If the subsequent Beige Ebook set for launch on April 23 at 14:00 ET is just like the prior one, the dangers of a recession grow to be noticeably increased.

Prior to now, there was a considerable lag between when the NBER introduced the turning factors within the economic system and when these really occurred. The NBER must have all the info after which analyze it totally. Understandably that takes time. Nonetheless, the info was unmistakable within the first months of the recession introduced on by the pandemic. The NBER referred to as the final recession on June 8, 2020 and put the height for the prior enlargement in February 2020. On July 19, 2021, the NBER mentioned the recession lasted a scant two months in March and April 2020.

The quick interval between when the NBER decided the recession begin/finish for the February-March 2020 downturn might be because of the overwhelming proof that wanted little nuanced interpretation. The current financial knowledge could also be a lot cloudier by way of precisely assessing whether or not the US is now in recession. The outlier in comparison with different downturns is principally the low unemployment price.

Share This Story, Select Your Platform!

Web page load hyperlink

")

{kind=link}