Up to date on April fifteenth, 2026 by Josh Arnold

ARMOUR Residential REIT Inc. (ARR) is a mortgage Actual Property Funding Belief (mREIT) that provides an interesting 19% dividend yield, making it a excessive dividend inventory.

ARMOUR Residential additionally pays its dividends month-to-month, which is uncommon. The overwhelming majority of corporations that pay dividends pay them quarterly or semi-annually.

There are at present over 76 month-to-month dividend shares in our protection universe. You possibly can obtain our full checklist of 118 month-to-month dividend shares (together with price-to-earnings ratios, dividend yields, and payout ratios) by clicking on the hyperlink under:

ARMOUR Residential’s excessive dividend yield and month-to-month dividend funds make it an intriguing inventory for traders, regardless that its dividend funds have declined through the years.

As with many high-dividend shares yielding over 10%, the sustainability of the dividend is in query. This text will analyze the funding prospects of ARMOUR Residential.

Enterprise Overview

As an mREIT, ARMOUR Residential invests in residential mortgage-backed securities, together with these issued or assured by U.S. Authorities-sponsored entities (GSE) resembling Fannie Mae and Freddie Mac. It additionally consists of Ginnie Mae, the Authorities Nationwide Mortgage Administration’s issued or assured securities backed by fixed-rate, hybrid adjustable-rate, and adjustable-rate dwelling loans.

It additionally consists of unsecured notes and bonds issued by the GSE and the USA treasuries, cash market devices, and non-GSE or authorities agency-backed securities.

The mortgage REIT, based in 2008 and primarily based in Vero Seaside, Florida, seeks to create shareholder worth via cautious funding and threat administration practices that produce present yield and superior risk-adjusted returns over the long run.

With a market cap of roughly $2.2 billion and annual income of $250 million, it’s a important nationwide participant in residential funding.

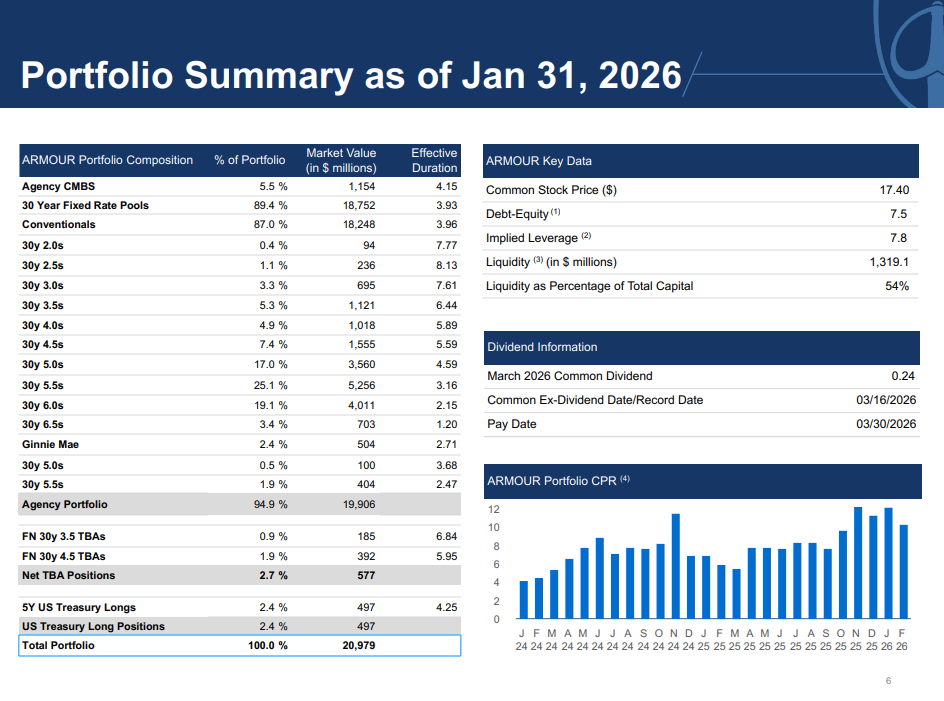

Supply: Investor presentation

The belief makes cash by elevating capital by issuing debt, most popular fairness, and customary fairness after which reinvesting the proceeds into higher-yielding debt devices.

The unfold (i.e., the distinction between the price of capital and the return on capital) is then largely returned to widespread shareholders by way of dividend funds. Nevertheless, the belief typically retains somewhat little bit of the income to reinvest within the enterprise. We be aware that the belief’s skill to generate unfold is considerably out of its management, relying upon market situations.

Development Prospects

Current outcomes at ARMOUR have been blended because it navigates between difficult and favorable rate of interest unfold situations. The COVID-19 pandemic severely impacted the belief, nevertheless it may meet all of its margin calls and preserve entry to repurchase financing.

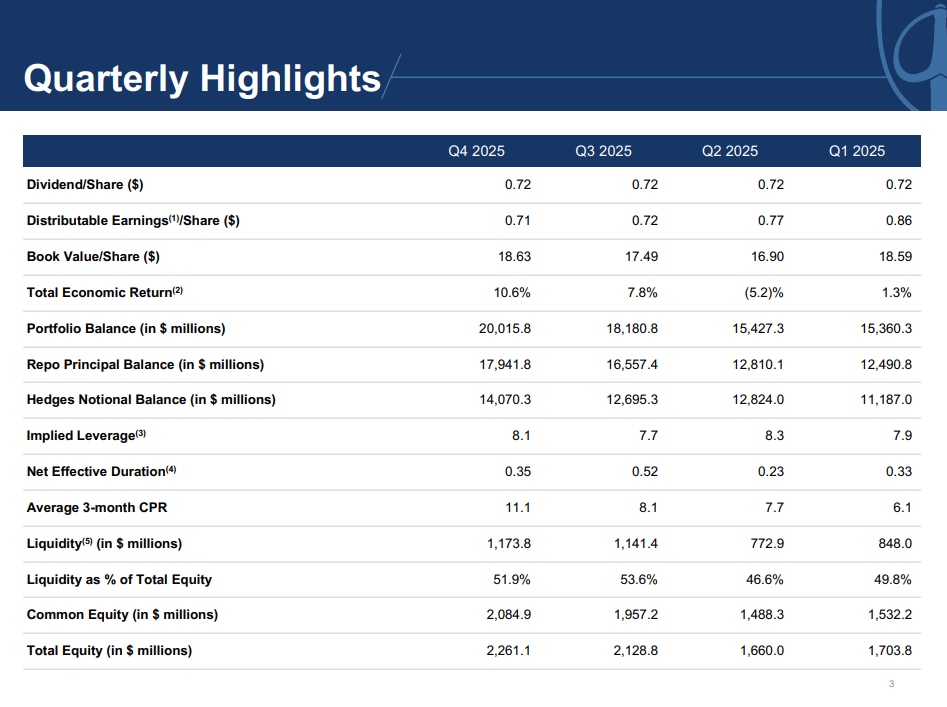

Armour posted fourth quarter and full-year earnings on February 18th, 2026, and outcomes had been challenged. Distributable earnings-per-share fell 9% year-over-year for the quarter, lacking estimates. The decline was primarily attributable to a a lot greater share rely, in addition to a lot greater compensation charges. The share rely almost doubled in 2025, creating a large headwind to earnings-per-share. Reimbursement charges additionally jumped from 8.7% in This autumn 2024 to 11.1% in the newest quarter.

Guide worth per share declined 2.3% year-over-year to $18.63.

Supply: Investor presentation

ARMOUR’s money move has been risky since its inception in 2008, however that is to be anticipated with all mREITs. Of late, declining spreads have damage earnings whereas the financial disruption brought on by the coronavirus outbreak disrupted the enterprise mannequin, resulting in a pointy decline in money move per share, in addition to a steep dividend lower. We see the belief’s fundamentals persevering with to wrestle, and we expect FFO-per-share may fall by greater than 11% yearly over the following 5 years. Certainly, the earnings declines we’ve seen in recent times aren’t one thing we consider ARMOUR can get well, leaving it in a spot the place its finest days are virtually actually behind it.

Threat Concerns

Whereas there have been some restricted optimistic developments at work for ARMOUR, there are nonetheless a number of dangers to be involved about. ARMOUR’s high quality metrics have been risky, given the belief’s efficiency as charges have moved round over the years. Gross margins have moved down since brief–time period charges started to rise meaningfully a few years in the past, though it seems most of that harm has been performed.

Stability sheet leverage had been moving down barely, however it noticed an uptick once more this previous few quarters. Nevertheless, we don’t forecast a important motion in both course from this level. Curiosity protection has declined with spreads but additionally seems to have stabilized, so we’re considerably optimistic transferring ahead whereas conserving in thoughts the numerous potential for volatility. We be aware compensation charges proceed to maneuver greater and haven’t plateaued as of the tip of the fourth quarter 2025.

ARMOUR was dealing with headwinds from the coronavirus outbreak and an total financial downturn. Consequently, a steep dividend lower was essential to protect the steadiness sheet and permit the REIT to reposition itself for survival and future development.

The annualized dividend payout of $2.88 per share will characterize 98% of the corporate’s EPS (we estimate 2026 EPS of $2.95). This can be a concern because the payout ratio is extraordinarily excessive, and the dividend could possibly be prone to additional discount if EPS falls or stays at this stage for too lengthy.

For instance, if the financial system had been to enter recession, mortgage defaults may surge, resulting in steep losses. Given the unsure macroeconomic outlook, this threat is related for traders, significantly if rates of interest transfer rapidly.

Remaining Ideas

ARMOUR Residential’s excessive dividend yield and month-to-month dividend funds make it stand out to high-yield dividend traders. Nevertheless, we stay cautious on the inventory, particularly in gentle of the a number of dividend cuts in recent times, and really excessive payout ratio.

Whereas the belief can at present cowl its dividend, declining rates of interest may proceed to drive the belief ever additional out on the danger spectrum to take care of its money flows as its older mortgages roll off the steadiness sheet. This units it up for probably steep losses if the financial system had been to slide right into a recession.

Subsequently, ARMOUR inventory carries notably greater ranges of threat than most different earnings shares. This makes the funding extremely speculative proper now, particularly for risk-averse earnings traders resembling retirees. Consequently, we encourage risk-averse traders to look elsewhere for sustainable and rising earnings, and to not be drawn in by the large 16% dividend yield.

Don’t miss the assets under for extra month-to-month dividend inventory investing analysis.

And see the assets under for extra compelling funding concepts for dividend development shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

Discusses Energy Market Impacts and Supply Chain Disruptions from Iran Conflict Transcript")

Q4 2026 Earnings Call Transcript")

{kind=link}