Revealed on Might nineteenth, 2026 by Bob Ciura

Dividend shares are naturally interesting for revenue buyers, however not all dividend shares are buys.

Earnings buyers usually need to keep away from dividend cuts each time potential. Not solely does a dividend lower lead to a lack of revenue, however an organization’s share value sometimes declines after saying a dividend discount or suspension.

With this in thoughts, we compiled an inventory of excessive dividend shares with dividend yields above 5%. You’ll be able to obtain your free copy of the excessive dividend shares checklist by clicking on the hyperlink beneath:

The ten shares on this article all have Dividend Danger Scores of or ‘F’ (our lowest score) within the Certain Evaluation Analysis Database.

All 10 dangerous excessive dividend shares have promote rankings from Certain Dividend, primarily based on both deteriorating firm fundamentals, weak dividend protection, and/or an especially excessive valuation.

The checklist is sorted by annual anticipated returns over the subsequent 5 years.

Desk of Contents

You’ll be able to immediately bounce to any particular part of the article by utilizing the hyperlinks beneath:

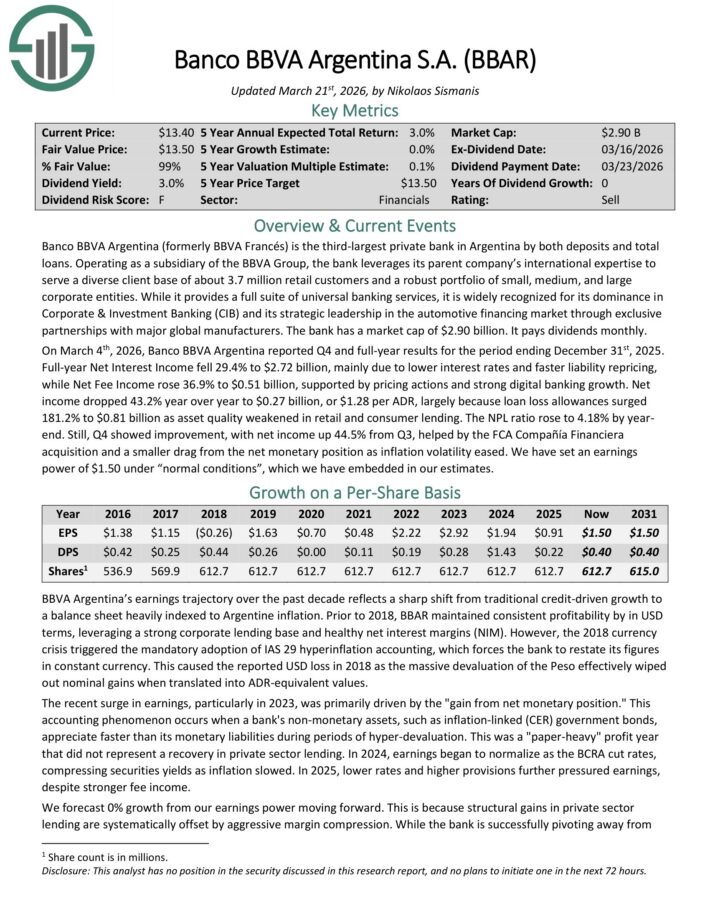

Excessive Danger Inventory To Promote Now #10: Banco BBVA Argentina S.A. (BBAR)

- Annual Anticipated Returns: 1.0%

Banco BBVA Argentina (previously BBVA Francés) is the third-largest personal financial institution in Argentina by each deposits and whole loans.

Working as a subsidiary of the BBVA Group, the financial institution leverages its guardian firm’s worldwide experience to serve a various consumer base of about 3.7 million retail clients and a sturdy portfolio of small, medium, and huge company entities.

Whereas it gives a full suite of common banking providers, it’s well known for its dominance in Company & Funding Banking (CIB) and its strategic management within the automotive financing market by unique partnerships with main international producers.

On March 4th, 2026, Banco BBVA Argentina reported This autumn and full-year outcomes for the interval ending December thirty first, 2025. Full-year Web Curiosity Earnings fell 29.4% to $2.72 billion, primarily resulting from decrease rates of interest and sooner legal responsibility repricing, whereas Web Payment Earnings rose 36.9% to $0.51 billion, supported by pricing actions and powerful digital banking progress.

Web revenue dropped 43.2% 12 months over 12 months to $0.27 billion, or $1.28 per ADR, largely as a result of mortgage loss allowances surged 181.2% to $0.81 billion as asset high quality weakened in retail and client lending. The NPL ratio rose to 4.18% by year-end.

Nonetheless, This autumn confirmed enchancment, with web revenue up 44.5% from Q3, helped by the FCA Compañía Financiera acquisition and a smaller drag from the web financial place as inflation volatility eased.

Click on right here to obtain our most up-to-date Certain Evaluation report on BBAR (preview of web page 1 of three proven beneath):

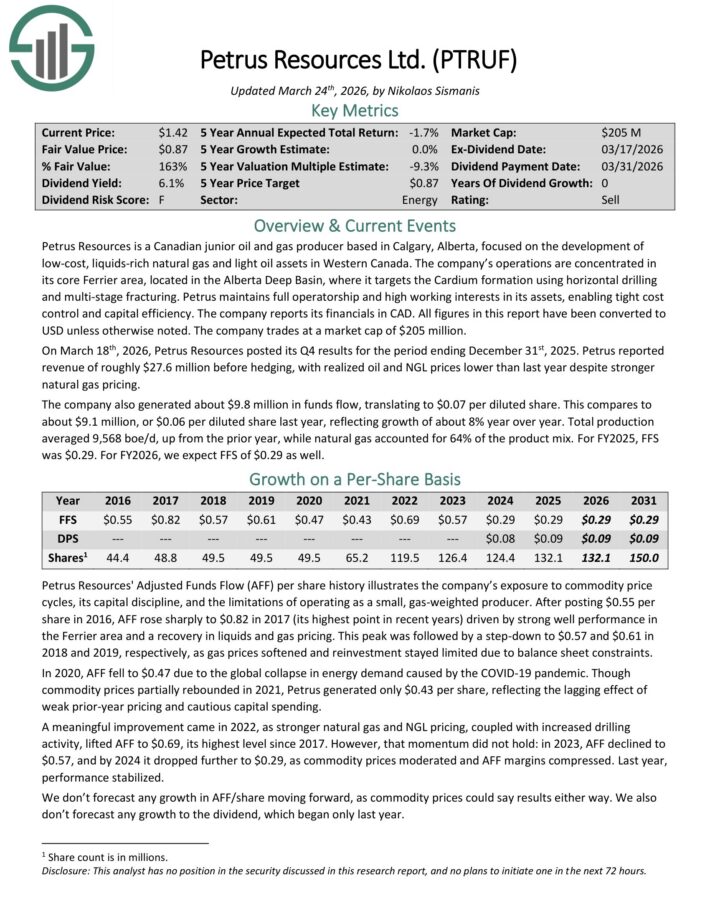

Excessive Danger Inventory To Promote Now #9: Petrus Assets Ltd. (PTRUF)

- Annual Anticipated Returns: 0.0%

Petrus Assets is a Canadian junior oil and gasoline producer primarily based in Calgary, Alberta, centered on the event of low-cost, liquids-rich pure gasoline and lightweight oil property in Western Canada.

The corporate’s operations are concentrated in its core Ferrier space, positioned within the Alberta Deep Basin, the place it targets the Cardium formation utilizing horizontal drilling and multi-stage fracturing.

Petrus maintains full operatorship and excessive working pursuits in its property, enabling tight price management and capital effectivity. The corporate experiences its financials in CAD.

On March 18th, 2026, Petrus Assets posted its This autumn outcomes for the interval ending December thirty first, 2025. Petrus reported income of roughly $27.6 million earlier than hedging, with realized oil and NGL costs decrease than final 12 months regardless of stronger pure gasoline pricing.

The corporate additionally generated about $9.8 million in funds move, translating to $0.07 per diluted share. This compares to about $9.1 million, or $0.06 per diluted share final 12 months, reflecting progress of about 8% 12 months over 12 months.

Complete manufacturing averaged 9,568 boe/d, up from the prior 12 months, whereas pure gasoline accounted for 64% of the product combine. For FY2025, FFS was $0.29.

Click on right here to obtain our most up-to-date Certain Evaluation report on PTRUF (preview of web page 1 of three proven beneath):

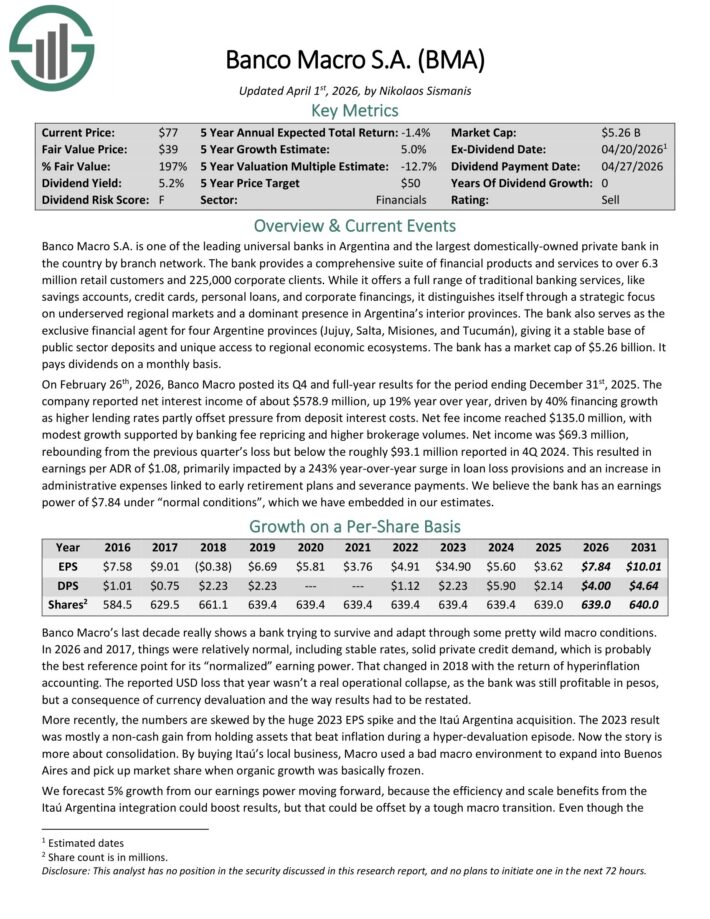

Excessive Danger Inventory To Promote Now #8: Banco Macro S.A. (BMA)

- Annual Anticipated Returns: -0.3%

Banco Macro S.A. is likely one of the main common banks in Argentina and the most important domestically-owned personal financial institution within the nation by department community.

The financial institution gives a complete suite of monetary services to over 6.3 million retail clients and 225,000 company purchasers.

On February twenty sixth, 2026, Banco Macro posted its This autumn and full-year outcomes for the interval ending December thirty first, 2025. The corporate reported web curiosity revenue of about $578.9 million, up 19% 12 months over 12 months, pushed by 40% financing progress as increased lending charges partly offset strain from deposit curiosity prices.

Web price revenue reached $135.0 million, with modest progress supported by banking price repricing and better brokerage volumes. Web revenue was $69.3 million, rebounding from the earlier quarter’s loss however beneath the roughly $93.1 million reported in 4Q 2024.

This resulted in earnings per ADR of $1.08, primarily impacted by a 243% year-over-year surge in mortgage loss provisions and a rise in administrative bills linked to early retirement plans and severance funds.

Click on right here to obtain our most up-to-date Certain Evaluation report on BMA (preview of web page 1 of three proven beneath):

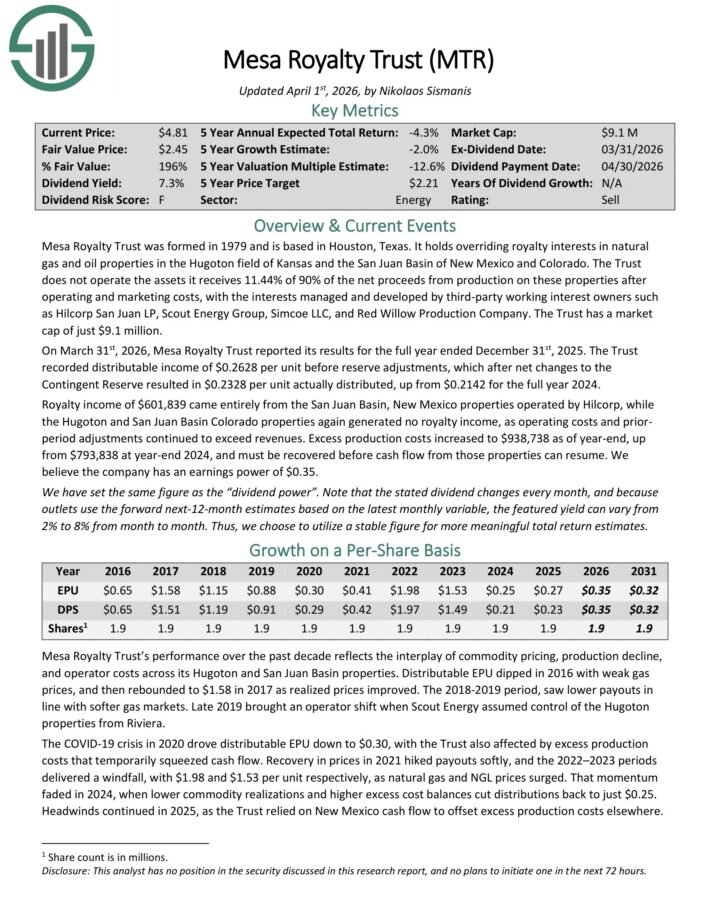

Excessive Danger Inventory To Promote Now #7: Mesa Royalty Belief (MTR)

- Annual Anticipated Returns: -0.9%

Mesa Royalty Belief was shaped in 1979 and relies in Houston, Texas. It holds overriding royalty pursuits in pure gasoline and oil properties within the Hugoton discipline of Kansas and the San Juan Basin of New Mexico and Colorado.

The Belief doesn’t function the property it receives 11.44% of 90% of the web proceeds from manufacturing on these properties after working and advertising prices, with the pursuits managed and developed by third-party working curiosity homeowners akin to Hilcorp San Juan LP, Scout Power Group, Simcoe LLC, and Crimson Willow Manufacturing Firm.

On March thirty first, 2026, Mesa Royalty Belief reported its outcomes for the complete 12 months ended December thirty first, 2025.

The Belief recorded distributable revenue of $0.2628 per unit earlier than reserve changes, which after web modifications to the Contingent Reserve resulted in $0.2328 per unit truly distributed, up from $0.2142 for the complete 12 months 2024.

Royalty revenue of $601,839 got here completely from the San Juan Basin, New Mexico properties operated by Hilcorp, whereas the Hugoton and San Juan Basin Colorado properties once more generated no royalty revenue, as working prices and prior interval changes continued to exceed revenues.

Extra manufacturing prices elevated to $938,738 as of year-end, up from $793,838 at year-end 2024, and should be recovered earlier than money move from these properties can resume.

On April twentieth, Mesa declared a $0.0402 per share share month-to-month dividend.

Click on right here to obtain our most up-to-date Certain Evaluation report on MTR (preview of web page 1 of three proven beneath):

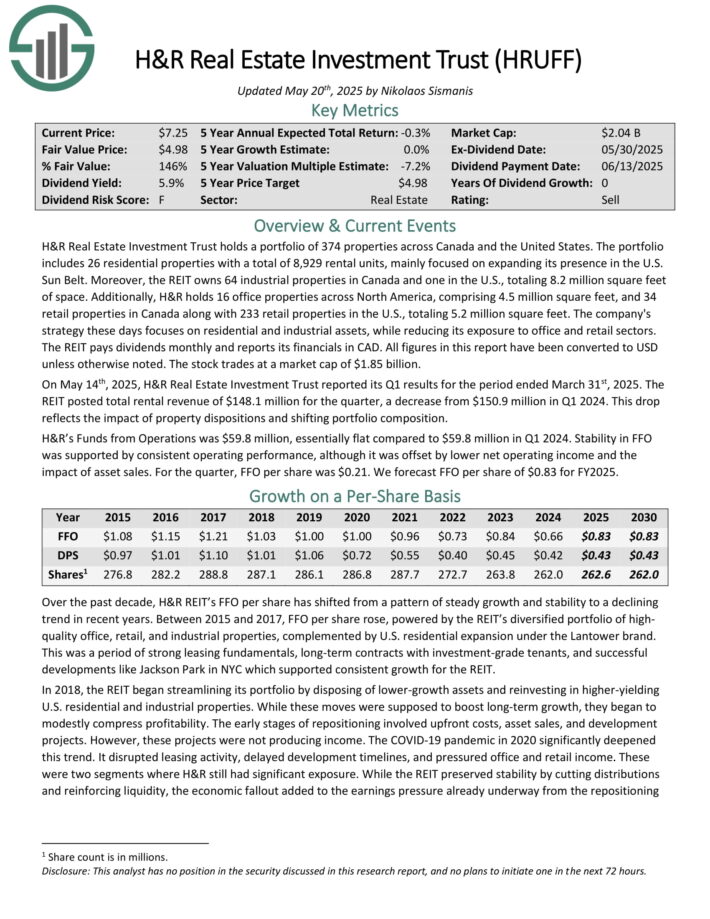

Excessive Danger Inventory To Promote Now #6: H&R Actual Property Funding Belief (HRUFF)

- Annual Anticipated Returns: -1.1%

H&R Actual Property Funding Belief holds a portfolio of 374 properties throughout Canada and the US.

The portfolio contains 26 residential properties with a complete of 8,929 rental items, primarily centered on increasing its presence within the U.S. Solar Belt.

Furthermore, the REIT owns 64 industrial properties in Canada and one within the U.S., totaling 8.2 million sq. toes of area.

Moreover, H&R holds 16 workplace properties throughout North America, comprising 4.5 million sq. toes, and 34 retail properties in Canada together with 233 retail properties within the U.S., totaling 5.2 million sq. toes.

The corporate’s technique nowadays focuses on residential and industrial property, whereas lowering its publicity to workplace and retail sectors.

The REIT pays dividends month-to-month and experiences its financials in CAD.

Click on right here to obtain our most up-to-date Certain Evaluation report on HRUFF (preview of web page 1 of three proven beneath):

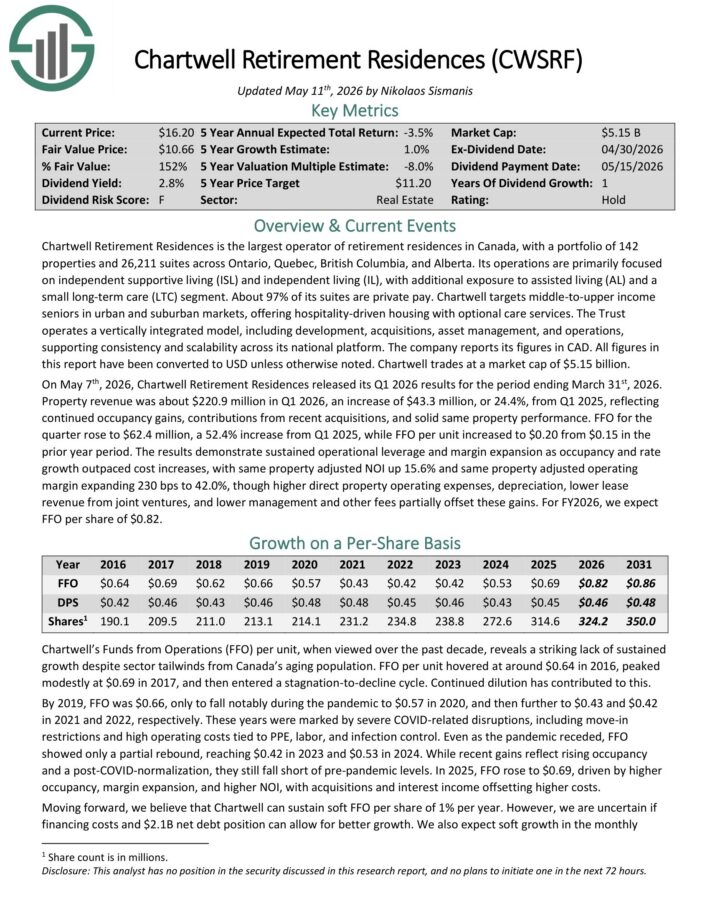

Excessive Danger Inventory To Promote Now #5: Chartwell Retirement Residences (CWSRF)

- Annual Anticipated Returns: -2.2%

Chartwell Retirement Residences is the most important operator of retirement residences in Canada, with a portfolio of 142 properties and 26,211 suites throughout Ontario, Quebec, British Columbia, and Alberta.

Its operations are primarily centered on unbiased supportive residing (ISL) and unbiased residing (IL), with extra publicity to assisted residing (AL) and a small long-term care (LTC) phase.

About 97% of its suites are personal pay. Chartwell targets middle-to-upper revenue seniors in city and suburban markets, providing hospitality-driven housing with non-compulsory care providers.

On Might seventh, 2026, Chartwell Retirement Residences launched its Q1 2026 outcomes for the interval ending March thirty first, 2026. Property income was about $220.9 million in Q1 2026, a rise of $43.3 million, or 24.4%, from Q1 2025, reflecting continued occupancy features, contributions from current acquisitions, and stable similar property efficiency.

FFO for the quarter rose to $62.4 million, a 52.4% improve from Q1 2025, whereas FFO per unit elevated to $0.20 from $0.15 within the prior 12 months interval.

Click on right here to obtain our most up-to-date Certain Evaluation report on CWSRF (preview of web page 1 of three proven beneath):

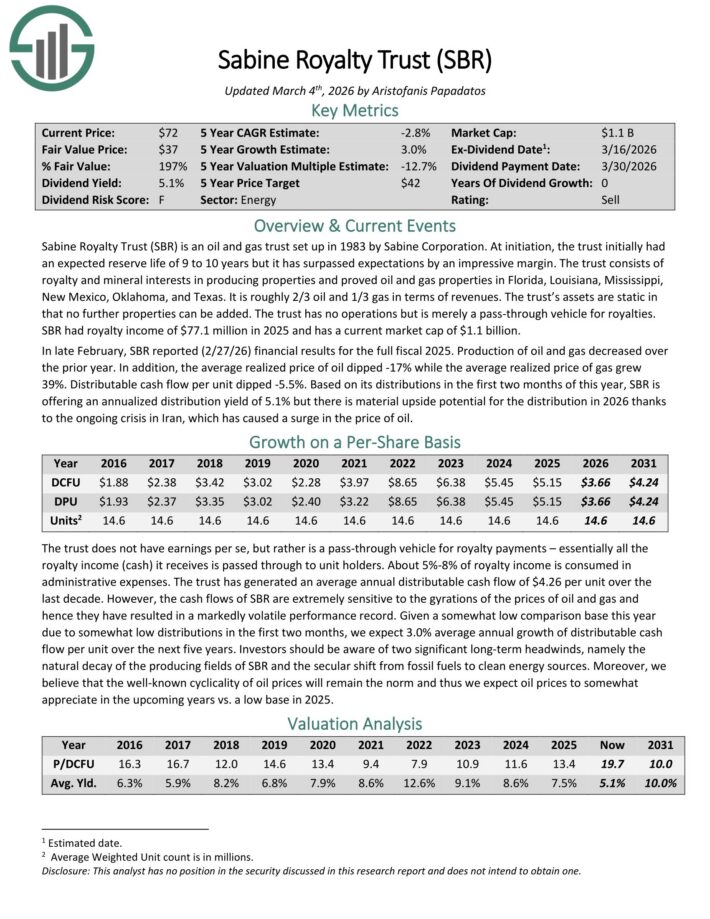

Excessive Danger Inventory To Promote Now #4: Sabine Royalty Belief (SBR)

- Annual Anticipated Returns: -4.2%

Sabine Royalty Belief (SBR) is an oil and gasoline belief arrange in 1983 by Sabine Company. At initiation, the belief initially had an anticipated reserve lifetime of 9 to 10 years however it has surpassed expectations by a formidable margin.

The belief consists of royalty and mineral pursuits in producing properties and proved oil and gasoline properties in Florida, Louisiana, Mississippi, New Mexico, Oklahoma, and Texas. It’s roughly 2/3 oil and 1/3 gasoline when it comes to revenues.

The belief’s property are static in that no additional properties could be added. The belief has no operations however is merely a move by car for royalties. SBR had royalty revenue of $82.6 million in 2024 and has a present market cap of $965 million.

In late February, SBR reported (2/27/26) monetary outcomes for the complete fiscal 2025. Manufacturing of oil and gasoline decreased over the prior 12 months.

As well as, the common realized value of oil dipped -17% whereas the common realized value of gasoline grew 39%. Distributable money move per unit dipped -5.5%.

Click on right here to obtain our most up-to-date Certain Evaluation report on SBR (preview of web page 1 of three proven beneath):

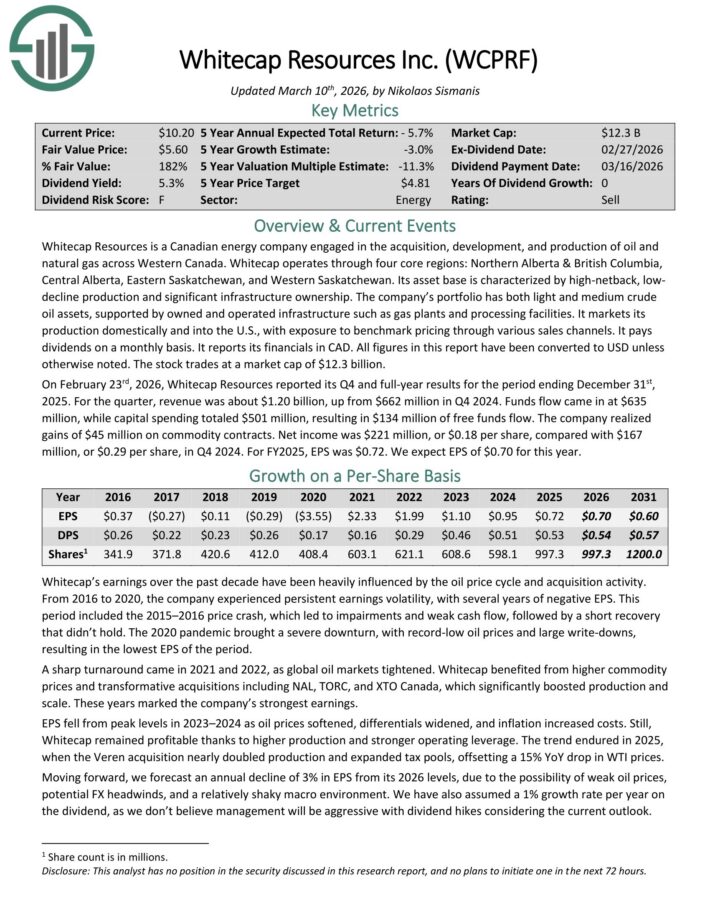

Excessive Danger Inventory To Promote Now #3: Whitecap Assets (WCPRF)

- Annual Anticipated Returns: -4.7%

Whitecap Assets is a Canadian power firm engaged within the acquisition, growth, and manufacturing of oil and pure gasoline throughout Western Canada.

Whitecap operates by 4 core areas: Northern Alberta & British Columbia, Central Alberta, Jap Saskatchewan, and Western Saskatchewan.

It markets its manufacturing domestically and into the U.S., with publicity to benchmark pricing by numerous gross sales channels. It pays dividends on a month-to-month foundation.

On Might twelfth, 2025, Whitecap Assets efficiently accomplished its strategic mixture with Veren, making it Canada’s seventh largest oil and pure gasoline producer and fifth largest pure gasoline producer.

The merger additionally positioned Whitecap as the most important landholder in Alberta’s Montney and Duvernay performs and a number one gentle oil producer in Saskatchewan. On July ninth, 2025, Whitecap Assets modified its OTC ticker from SPGYF to WCPRF after upgrading to the OTCQX.

On February twenty third, 2026, Whitecap Assets reported its This autumn and full-year outcomes for the interval ending December thirty first, 2025. For the quarter, income was about $1.20 billion, up from $662 million in This autumn 2024.

Funds move got here in at $635 million, whereas capital spending totaled $501 million, leading to $134 million of free funds move. The corporate realized features of $45 million on commodity contracts.

Web revenue was $221 million, or $0.18 per share, in contrast with $167 million, or $0.29 per share, in This autumn 2024. For FY2025, EPS was $0.72.

Click on right here to obtain our most up-to-date Certain Evaluation report on WCPRF (preview of web page 1 of three proven beneath):

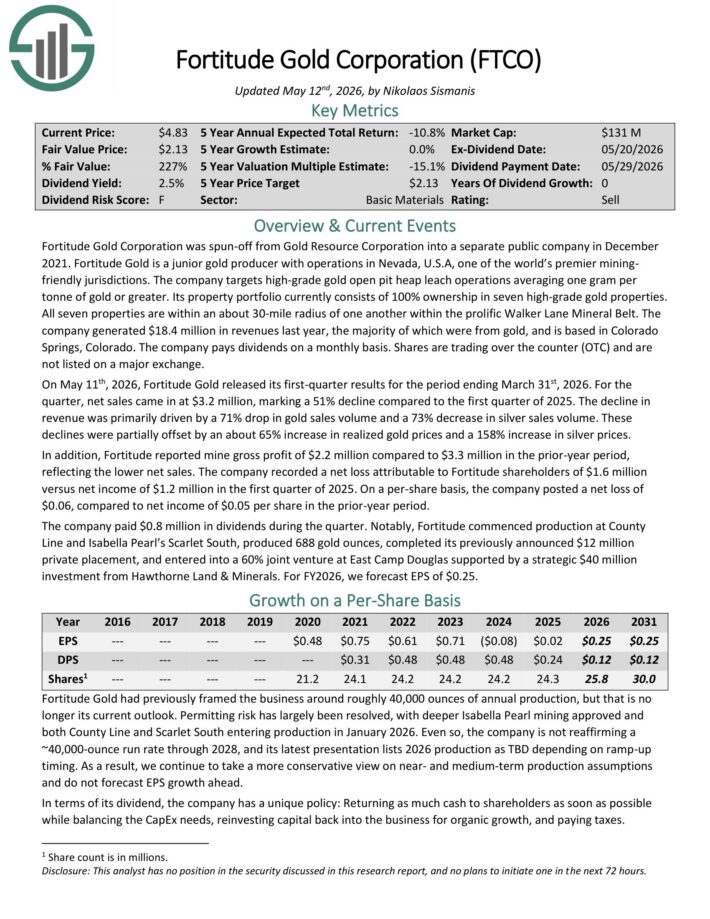

Dangerous Excessive Dividend Inventory #2: Fortitude Gold Corp. (FTCO)

- Annual Anticipated Returns: -10.8%

Fortitude Gold is a junior gold producer with operations in Nevada, U.S.A, one of many world’s premier mining-friendly jurisdictions.

The corporate targets high-grade gold open pit heap leach operations averaging one gram per tonne of gold or better.

Its property portfolio presently consists of 100% possession in seven high-grade gold properties. All seven properties are inside an about 30-mile radius of each other throughout the prolific Walker Lane Mineral Belt.

The corporate generated $18.4 million in revenues final 12 months, nearly all of which had been from gold, and relies in Colorado Springs, Colorado.

On Might eleventh, 2026, Fortitude Gold launched its first-quarter outcomes for the interval ending March thirty first, 2026. For the quarter, web gross sales got here in at $3.2 million, marking a 51% decline in comparison with the primary quarter of 2025.

The decline in income was primarily pushed by a 71% drop in gold gross sales quantity and a 73% lower in silver gross sales quantity. These declines had been partially offset by an about 65% improve in realized gold costs and a 158% improve in silver costs.

As well as, Fortitude reported mine gross revenue of $2.2 million in comparison with $3.3 million within the prior-year interval, reflecting the decrease web gross sales.

The corporate recorded a web loss attributable to Fortitude shareholders of $1.6 million versus web revenue of $1.2 million within the first quarter of 2025.

On a per-share foundation, the corporate posted a web lack of $0.06, in comparison with web revenue of $0.05 per share within the prior-year interval.

Click on right here to obtain our most up-to-date Certain Evaluation report on FTCO (preview of web page 1 of three proven beneath):

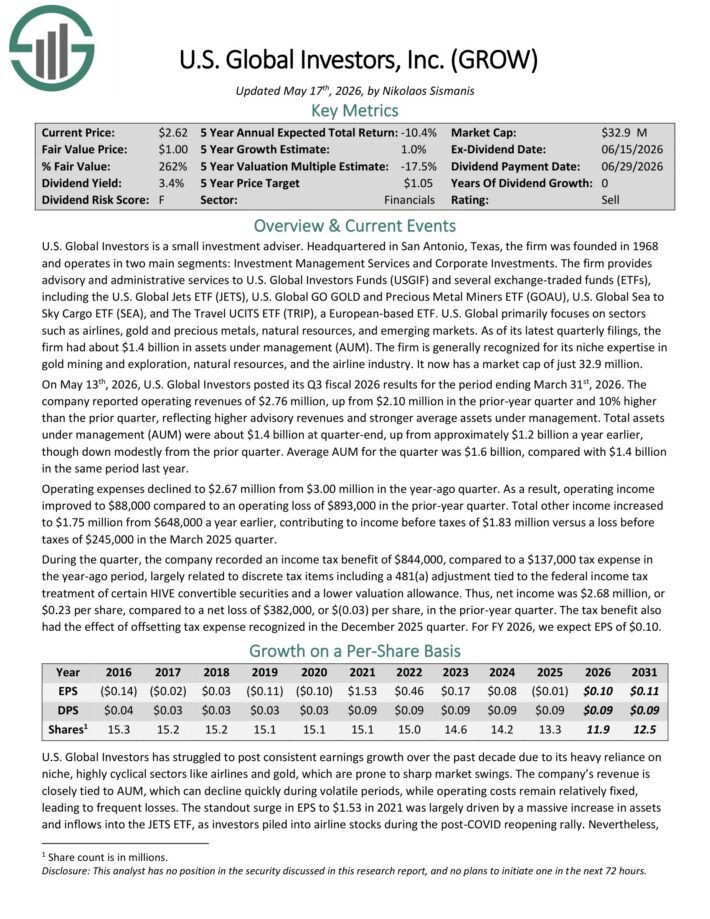

Dangerous Excessive Dividend Inventory #1: U.S. World Buyers (GROW)

- Annual Anticipated Returns: -11.2%

U.S. World Buyers is a small funding adviser. The agency operates in two major segments: Funding Administration Companies and Company Investments.

The agency gives advisory and administrative providers to U.S. World Buyers Funds (USGIF) and several other trade traded funds (ETFs), together with the U.S. World Jets ETF (JETS), U.S. World GO GOLD and Valuable Steel Miners ETF (GOAU), U.S. World Sea to Sky Cargo ETF (SEA), and The Journey UCITS ETF (TRIP), a European-based ETF.

U.S. World primarily focuses on sectors akin to airways, gold and treasured metals, pure sources, and rising markets. As of its newest quarterly filings, the agency had about $1.4 billion in property below administration (AUM).

On Might thirteenth, 2026, U.S. World Buyers posted its Q3 fiscal 2026 outcomes for the interval ending March thirty first, 2026. The corporate reported working revenues of $2.76 million, up from $2.10 million within the prior-year quarter and 10% increased than the prior quarter, reflecting increased advisory revenues and stronger common property below administration.

Complete property below administration (AUM) had been about $1.4 billion at quarter-end, up from roughly $1.2 billion a 12 months earlier, although down modestly from the prior quarter.

Click on right here to obtain our most up-to-date Certain Evaluation report on GROW (preview of web page 1 of three proven beneath):

Extra Studying

If you’re concerned about discovering high-quality dividend progress shares and/or different high-yield securities and revenue securities, the next Certain Dividend sources shall be helpful:

Excessive-Yield Particular person Safety Analysis

Different Certain Dividend Assets

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

Is a Retention Story, Not Just a Jobs Proxy – Alphastreet")

{kind=link}