Up to date on July eighth, 2026 by Nathan Parsh

Solely one of the best firms can improve dividends via a number of recessions.

The Dividend Kings are a gaggle of shares which have elevated their dividends for a minimum of 50 consecutive years. Engaging in this process isn’t any small feat. The truth that solely 58 firms meet the requirement to turn into a Dividend King is proof of this.

You may see all 58 Dividend Kings right here.

You too can obtain an Excel spreadsheet with the total record of Dividend Kings (plus necessary metrics resembling price-to-earnings ratios and dividend yields) by clicking on the hyperlink under:

Johnson & Johnson (JNJ) has elevated its dividend for 64 consecutive years, one of many longest dividend progress streaks within the inventory market.

This healthcare big is likely one of the hottest dividend progress shares resulting from its wonderful recession-resistant enterprise mannequin and robust dividend observe file.

Johnson & Johnson inventory stays a superb holding for long-term dividend progress.

Enterprise Overview

Johnson & Johnson was based in 1886 and has remodeled into one of many largest firms on this planet. Johnson & Johnson is a mega-cap inventory with a market capitalization of $640 billion. The corporate generates annual gross sales of $94 billion.

Johnson & Johnson operates a diversified enterprise mannequin, enabling it to enchantment to a broad vary of consumers inside the healthcare sector. J&J now operates two segments: prescription drugs and medical units, following the spin-off of its shopper well being companies.

Development Prospects

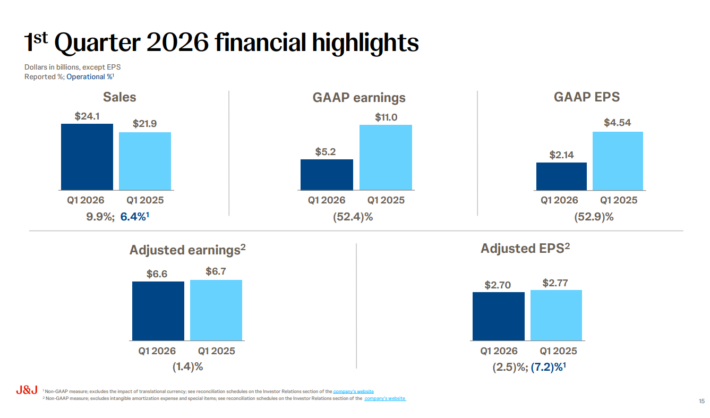

Johnson & Johnson reported first-quarter outcomes on April 14th, 2026.

Supply: Investor Presentation

For the interval, income elevated almost 10% to $24.1 billion, which beat estimates by $450 million. Adjusted earnings-per-share of $2.70 was down from $2.77 within the prior 12 months, however this was $0.20 higher than anticipated.

Regionally, U.S. gross sales elevated by 8.3%, whereas worldwide markets had been up 11.9%, leading to 9.9% progress in complete worldwide gross sales. Adjusting for forex change, income grew 6.4% worldwide.

The Modern Medication phase reported 7.4% currency-neutral progress, pushed by power in oncology and neuroscience, offset by weaker ends in immunology. MedTech grew 4.6% as all product classes had been greater for the interval, with cardiovascular main the best way with double-digit gross sales progress.

Johnson & Johnson revised its full-year 2026 steering to replicate higher operational efficiency. The corporate anticipates adjusted EPS to be within the vary of $11.45 to $11.65, up from the beforehand reported vary of $11.28 to $11.48. This might signify 7% progress on the midpoint. Gross sales for 2026 are anticipated to develop between 5.6% and 6.6%, demonstrating administration’s confidence in sustained progress.

Supply: Investor Presentation

We count on Johnson & Johnson to generate 6% annual earnings-per-share progress over the subsequent 5 years. The pharmaceutical phase will proceed to be the corporate’s principal progress driver, because it has for a number of years.

Aggressive Benefits & Recession Efficiency

Johnson & Johnson has a number of benefits over its rivals.

Johnson & Johnson’s measurement and scale are unmatched in its business. It additionally has a AAA credit standing from Customary & Poor’s and Moody’s Buyers Service, which is greater than the U.S. authorities’s.

Microsoft Company (MSFT) is the one different firm with an AAA credit standing.

The corporate’s measurement and scale, together with its credit standing, present Johnson & Johnson with the monetary flexibility to make acquisitions that gasoline additional progress.

Johnson & Johnson additionally invests closely in analysis and improvement to deliver new merchandise to market. This funding has resulted within the firm’s in depth portfolio of manufacturers that lead their respective classes.

These aggressive benefits allowed Johnson & Johnson to climate a number of recessions. Listed under are the corporate’s earnings-per-share outcomes earlier than, throughout, and after the final main recession:

- 2006 earnings-per-share: $3.76

- 2007 earnings-per-share: $4.15 (9.4% improve)

- 2008 earnings-per-share: $4.57 (10.1% improve)

- 2009 earnings-per-share: $4.63 (1.3% improve)

- 2010 earnings-per-share: $4.76 (2.8% improve)

Johnson & Johnson had EPS progress of just about 12% from 2007 via 2009, a formidable accomplishment given the circumstances of the Nice Recession.

The corporate’s dividend additionally continued to develop. With greater than six many years of dividend progress, Johnson & Johnson is more likely to proceed rising its dividend properly into the longer term. Moreover, the spinoff of its shopper enterprise has allowed Johnson & Johnson to deal with the expansion facets of its enterprise, which may result in improved outcomes and a better a number of from the market.

Johnson & Johnson’s aggressive benefits and recession efficiency make the inventory a superb defensive inventory.

Valuation & Anticipated Returns

With a present share worth of $266 and anticipated earnings per share of $11.55 for the 12 months, Johnson & Johnson has a price-to-earnings ratio of 23.0.

We view the inventory as barely overvalued, with a good worth P/E estimate of 17. A number of contraction to 17 from 23 may cut back annual returns by 2.1% over the subsequent 5 years.

Complete returns will even include earnings progress and dividends.

Given the corporate’s aggressive benefits and up to date enterprise efficiency, we really feel {that a} 6% common annual EPS progress price is achievable over the subsequent 5 years.

Lastly, Johnson & Johnson inventory has a present dividend yield of two.0%. Due to this fact, complete annual returns are anticipated to be 2.1% yearly via 2030.

Ultimate Ideas

Few Dividend Kings are as well-known or fashionable amongst dividend progress buyers as Johnson & Johnson.

For good cause, Johnson & Johnson’s diversified enterprise mannequin has enabled the corporate to endure a number of recessions whereas nonetheless rising its dividends for the previous 64 years. This progress streak is sort of unmatched.

That being stated, the inventory is buying and selling above our goal a number of, which may imply {that a} valuation headwind may cap complete returns over the medium-term. For that cause, we price shares of Johnson & Johnson as a maintain.

The next articles include shares with very lengthy dividend or company histories, ripe for choice for dividend progress buyers:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

")

")

{kind=link}