State Financial institution of India (SBI) Chairman Challa Sreenivasulu Setty, addressing a media convention in Mumbai on Friday

| Photograph Credit score:

PTI

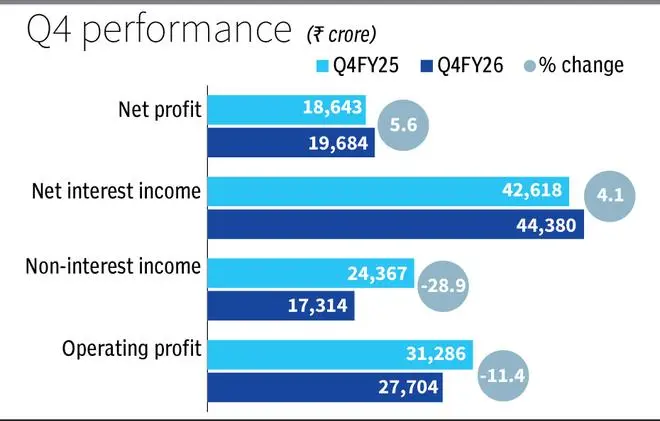

State Financial institution of India (SBI) reported a modest 6 per cent year-on-year (yoy) improve in fourth quarter (Q4FY26) standalone internet revenue at ₹19,684 crore, with the bottomline being supported by a good progress in internet curiosity revenue and decrease complete provisions whilst treasury revenue declined and margins got here underneath strain.

The inventory of India’s largest financial institution, which reported a internet revenue of ₹18,643 crore within the year-ago quarter, declined 6.62 per cent to shut at ₹1019.55apiece over the earlier shut on BSE.

The financial institution’s board declared a dividend of ₹ 17.35 per fairness share (1735 per cent) for FY26. In FY26, SBI reported a 13 per cent y-o-y improve in standalone internet revenue at ₹80,032 crore towards ₹70,901 crore in FY25.

Challa Sreenivasulu Setty, Chairman, stated he retained a 13-15 per cent credit score progress for FY27 , with the company credit score pipeline being sturdy at ₹5.50 lakh crore and sure demand for loans of as much as ₹80,000 crore from MSMEs and the aviation sector underneath the Authorities’s Emergency Credit score Line Assure Scheme.

Referring to SBI’s home view that the repo price will proceed on the similar degree all through FY27, Setty stated: “We’re an asset combine change, particularly on the company aspect, as a result of we had some floating price loans which in all probability would now run off, and we could have the flexibility to cross on a few of the further prices which we’ve got on the deposit aspect.

And on the deposit rate of interest aspect, I don’t suppose there’s a lot room by way of additional slicing down. If the continual credit score progress price is at 13 to fifteen per cent, I believe none of us within the system can be able to chop the deposit charges.”

Within the reporting quarter, internet curiosity revenue (distinction between curiosity earned and curiosity expended) was up 4 per cent y-o-y to ₹44,380 crore (₹42,618 crore in Q4FY25).

Non-interest revenue, comprising payment revenue, treasury revenue, mortgage processing costs, fee on authorities enterprise and letter of credit score/ Financial institution assure, amongst others, declined 29 per cent y-o-y to ₹17,314 crore (₹24,367 crore). Treasury revenue was down ₹6,209 crore throughout the reporting quarter as in comparison with the previous quarter

Whole provisions have been down 37 per cent to ₹8,020 crore (₹12,643 crore). Inside this mortgage, loss and revenue tax provisions have been down 21 per cent yoy (at ₹3,140 crore) and 30 per cent (at ₹5,148 crore), respectively.

Web curiosity margin nudged decrease to 2.81 per cent towards 2.99 per cent within the year-ago interval.

Gross non-performing property (NPAs) place improved to 1.49 per cent of gross advances as at March-end 2026 towards 1.82 per cent as at March-end 2025. Web NPAs place improved too, to 0.39 per cent of internet advances towards 0.47 per cent.

Gross advances elevated by 17 per cent y-o-y to ₹49,32,627 crore as at March-end 2026, primarily on the again of led by SME (20.99 per cent), Agri (19.68 per cent), Retail Private (15.22 per cent) and company (14.83 per cent).

Whole deposits rose by 11.03 per cent y-o-y to face at ₹59,75,642 crore as of March-end 2026. Low-cost CASA (present account, financial savings account) deposits declined to 39.46 per cent of complete deposits towards 39.97 per cent within the year-ago quarter.

Revealed on Could 8, 2026

{kind=link}