AlphaStreet Newsdesk powered by AlphaStreet Intelligence

FY26 EPS steering – adjusted $1.03 – $1.09|Inventory $24.30 (+1.2%)

EPS YoY +8.1%|Rev YoY +14.9%|Internet Margin 4.2%

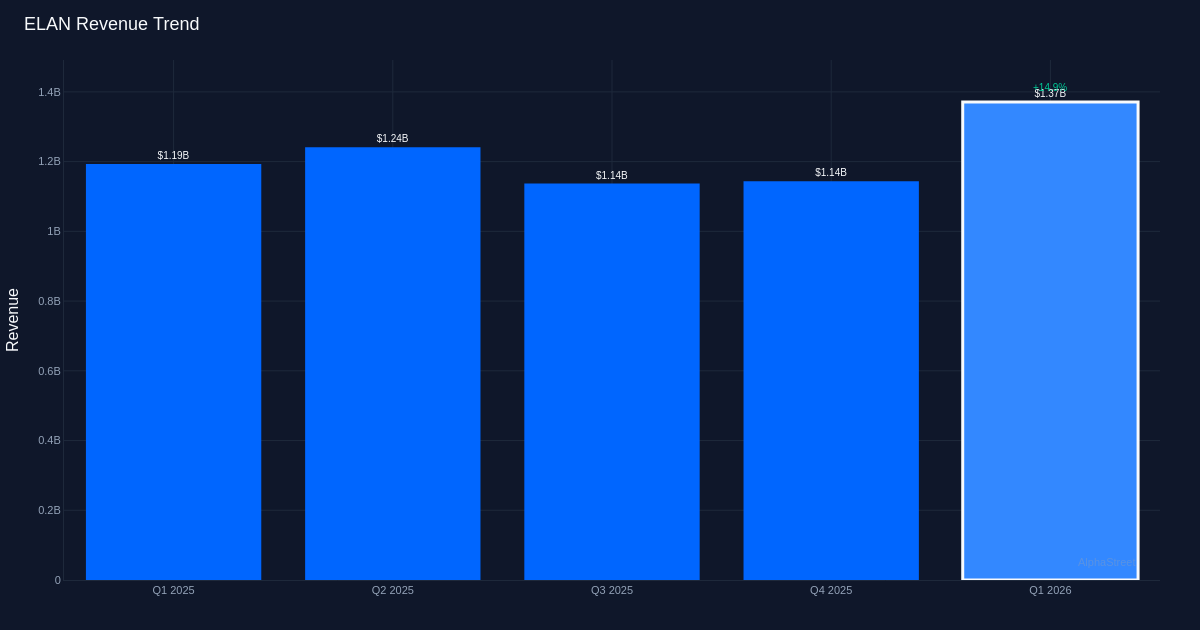

Elanco Animal Well being (ELAN) delivered a decisive beat in Q1 2026, posting adjusted EPS of $0.40 versus estimates of $0.35—a 14.3% shock—whereas income surged 15.0% year-over-year to $1.37B. The efficiency marks a significant acceleration from the corporate’s current trajectory and positions administration to boost innovation product targets whereas reaffirming full-year steering. But beneath the headline power lies a important pressure: sturdy top-line momentum paired with important margin deterioration that warrants nearer scrutiny from traders evaluating the sustainability of this progress.

Income progress got here at a significant profitability price, exposing potential high quality issues within the earnings beat. Whereas the 15.0% income growth represented the strongest quarter within the trailing four-period window, internet margin dropped to 4.2% from 5.6% within the year-ago interval—an 11.3 share level decline. Internet revenue declined to $57.0M from $67.0M, regardless of the income beneficial properties, suggesting the corporate sacrificed pricing energy or absorbed substantial enter price inflation to drive quantity. Gross margin of 57.3% and EBITDA of $334.0M present inadequate context with out year-ago comparables, however the internet margin decline signifies working leverage stays elusive. This isn’t cost-cutting self-discipline driving profitability—it’s revenue-at-any-cost growth that ought to concern value-focused traders.

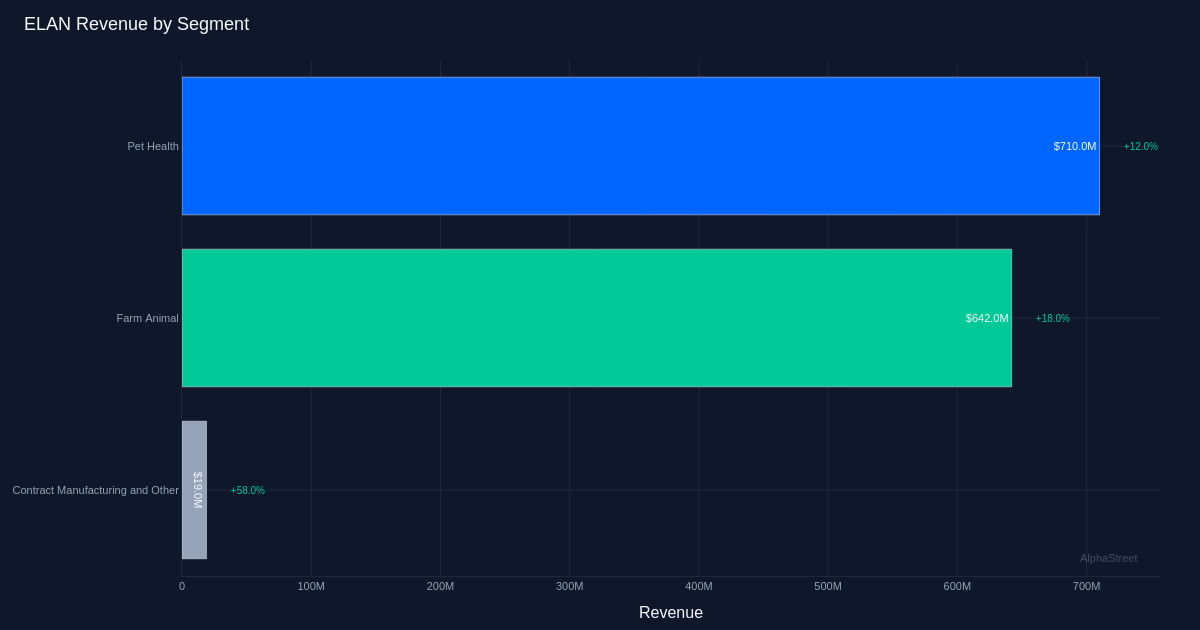

Farm Animal emerged because the sudden progress driver, outpacing the historically stronger Pet Well being section. The Farm Animal enterprise delivered $642.0M with 18.0% progress, considerably exceeding Pet Well being’s $710.0M and 12.0% growth. This divergence issues strategically—Pet Well being sometimes instructions greater margins and better pricing energy given shopper attachment to companion animals, whereas Farm Animal faces commodity-like pricing strain tied to agricultural economics. The 18.0% Farm Animal progress doubtless displays both restoration from prior-year weak point or destocking normalization reasonably than structural demand enchancment. Contract Manufacturing and Different posted $19.0M with explosive 58.0% progress, although the small absolute base limits materiality. Administration famous “the US pet well being end result within the quarter was up 6%,” suggesting worldwide markets drove the section’s 12.0% blended progress—a dynamic price monitoring given forex and regulatory dangers overseas.

Administration raised innovation product targets whereas sustaining conservative full-year steering, signaling confidence in particular product cycles however not broader margin restoration. Administration elevated the full-year innovation goal to $1.2B. It said: “After delivering $287 million of first quarter income from our innovation merchandise, we’re elevating our full 12 months innovation goal to $1.2 billion.” The maintained income steering of $5.01B to $5.08B implies sequential deceleration by the stability of 2026, as Q1 captured 27% of the midpoint goal regardless of representing simply 25% of the 12 months. Adjusted EPS steering of $1.03 to $1.09 with a $1.06 midpoint suggests important margin enchancment forward, as easy annualization of Q1’s $0.40 would suggest $1.60. This means both Q1 margin strain was short-term or administration expects seasonal headwinds—neither notably comforting given the year-ago margin compression already noticed.

Administration emphasised company account momentum as a number one indicator of sustained demand. Executives highlighted that “the variety of company accounts had been rising that weren’t rising final 12 months we noticed a 12% step up,” suggesting veterinary clinic consolidation and enterprise buyer wins are driving distribution beneficial properties. This issues as a result of company accounts sometimes provide extra predictable quantity however better pricing self-discipline. Administration additionally said: “We now anticipate natural fixed forex progress of 5 to 7%, adjusted EBITDA of 975 million to $1.005 billion representing 10% on the midpoint and adjusted EPS of $1.03 to $1.09 representing 13% progress on the midpoint.” The narrower natural progress steering of 5-7% versus Q1’s 10.0% precise efficiency confirms administration views the quarter as peak reasonably than inflection.

The inventory’s muted 1.2% acquire to $24.30 suggests traders are balancing the headline beat towards margin deterioration and conservative steering. A beat of this magnitude would sometimes command stronger value motion, however the market seems centered on earnings high quality reasonably than merely surpassing lowered expectations. The corporate now maintains a 100% beat price during the last quarter—although the single-quarter pattern supplies restricted predictive worth. The restrained response signifies traders want proof that income progress can translate into sustainable revenue growth earlier than rerating the fairness.

What to Watch: Q2 internet margin trajectory will decide whether or not Q1’s compression was short-term or structural—traders ought to demand at minimal a return towards mid-single-digit margins to validate the expansion story. Innovation product contribution to whole income and whether or not the $1.2B annual goal maintains momentum past Q1’s seasonal power. Farm Animal section sustainability as agricultural commodity costs fluctuate and whether or not Pet Well being can speed up from its 6% US progress price.

This content material is for informational functions solely and shouldn’t be thought of funding recommendation. AlphaStreet Intelligence analyzes monetary knowledge utilizing AI to ship quick and correct market data. Human editors confirm content material.

")

Data Center Revenue Hits .8 Billion; Q1 Beat Drives a Stronger Q2 Outlook – Alphastreet")

")

{kind=link}