Up to date on April fifteenth, 2026 by Nathan Parsh

Bridgemarq Actual Property Providers (BREUF) has two interesting funding traits:

#1: It’s a high-yield inventory based mostly on its 9.9% dividend yield.

Associated: Listing of 5%+ yielding shares.

#2: It pays dividends month-to-month as a substitute of quarterly.

Associated: Listing of month-to-month dividend shares

You may obtain our full Excel spreadsheet of all 118 month-to-month dividend shares (together with metrics that matter, like dividend yield and payout ratio) by clicking on the hyperlink beneath:

Combining a excessive dividend yield and a month-to-month dividend makes Bridgemarq Actual Property Providers interesting to income-oriented traders. The corporate additionally has a robust enterprise mannequin, with most of its revenues being recurring. On this article, we are going to talk about the prospects of Bridgemarq Actual Property Providers.

Enterprise Overview

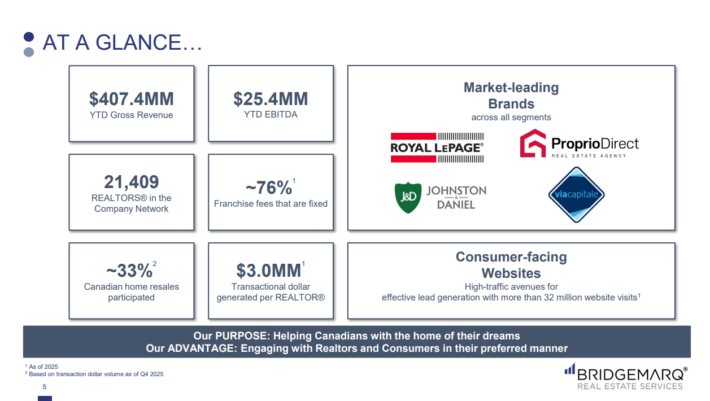

Bridgemarq Actual Property Providers supplies varied companies to residential actual property brokers and REALTORS in Canada. It gives data, instruments, and companies that help its clients within the supply of actual property companies. The corporate supplies its companies underneath the Royal LePage, Through Capitale, Johnston, and Daniel model names. The corporate was previously referred to as Brookfield Actual Property Providers and altered its title to Bridgemarq Actual Property Providers in 2019. Bridgemarq Actual Property Providers was based in 2010 and is headquartered in Toronto, Canada.

Bridgemarq generates money move from mounted and variable franchise charges from a nationwide community of greater than 21,000 REALTORS working underneath the aforementioned model names. Roughly 81% of the franchise charges are mounted in nature, leading to pretty predictable and dependable money flows. Franchise payment revenues are protected by way of long-term contracts.

Bridgemarq has a strong enterprise relationship with its companions, and thus, it enjoys remarkably excessive renewal charges. The corporate has traditionally achieved a 96% renewal price at any time when a contract has expired.

Supply: Investor Presentation

Furthermore, Royal LePage’s franchise agreements, which comprise 96% of the corporate’s REALTORS, are 10-to 20-year contracts, offering nice money move visibility.

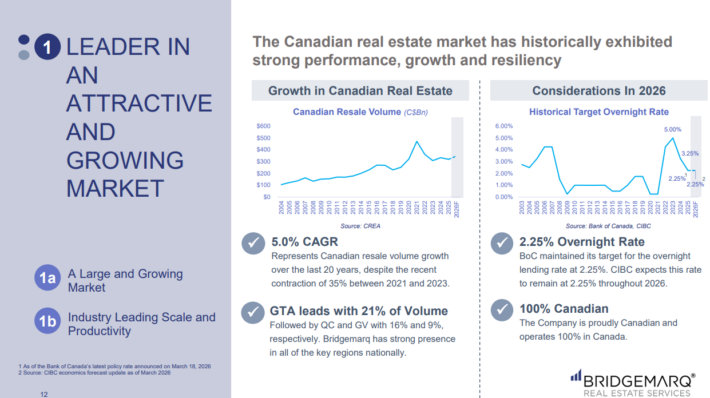

Bridgemarq has a dominant enterprise place in Canada. By means of its immense community of REALTORS, the corporate participated in over 70% of the whole dwelling resales in Canada. Bridgemarq’s manufacturers entice franchisees because of their status and the technological benefits they supply.

Regardless of its sturdy enterprise mannequin, Bridgemarq was severely harm by the fierce recession attributable to the coronavirus disaster in 2020. The Canadian actual property market confronted an unprecedented downturn that 12 months. Consequently, the corporate noticed its earnings per share plunge 47%, from $0.34 in 2019 to $0.18 in 2020.

On March thirteenth, 2026, Bridgemarq Actual Property Providers reported fourth-quarter and full-year outcomes for the interval ending December thirty first, 2025. Income for the quarter fell 2.9% to $69.6 million, because of a 16% year-over-year contraction within the Canadian residential market and decrease transaction volumes in Toronto and Vancouver.

Bridgemarq recorded a quarterly internet earnings of $0.38 per share, a big turnaround from the lack of $0.68 a 12 months earlier, primarily pushed by a non-cash achieve on the valuation of exchangeable items. Adjusted EPS for the quarter was a lack of $0.05, down from a lack of $0.02 final 12 months, as increased fee and working bills and elevated earnings tax prices outweighed the optimistic affect of strategic payment will increase and a 2% development within the agent community.

For the total 12 months, Bridgemarq generated earnings-per-share of $0.32, supported by a resilient community of 21,409 realtors regardless of broader business headwinds. We anticipate that the corporate will produce adjusted EPS of $1.00 this 12 months, which we have now utilized in our estimates.

Development Prospects

Bridgemarq pursues development by constantly rising the variety of its companions.

Supply: Investor Presentation

The corporate has grown the variety of REALTORS by greater than 6% since 2020. Consequently, it now has 21,409 companions working via 286 franchise agreements at 727 areas.

As talked about, the overwhelming majority of Bridgemarq’s franchise charges are mounted, which renders the corporate’s money flows pretty predictable. Nonetheless, that is simpler mentioned than finished.

Bridgemarq has exhibited a considerably risky efficiency document over the past 9 years because of the volatility in the actual property market and the swings of the trade price between the Canadian greenback and the USD.

Given Bridgemarq’s sturdy enterprise place, long-term efficiency document, and a few development limitations because of the firm’s dimension, we anticipate roughly 0.0% common annual earnings per share development over the following 5 years.

Dividend & Valuation Evaluation

Bridgemarq is providing an exceptionally excessive dividend yield of 9.9%, greater than eight instances the 1.2% yield of the S&P 500. The inventory is thus an attention-grabbing candidate for income-oriented traders, however U.S. traders must be conscious that the dividend they obtain is affected by the prevailing trade price between the Canadian greenback and the U.S. greenback.

Bridgemarq has routinely had payout ratio of over 100%, with final 12 months’s payout ratio equating to 306%. The projected payout ratio for 2026 is 98%. The corporate’s steadiness sheet doesn’t look excellent. The corporate’s internet debt is $67 million which compares to the inventory’s market capitalization of $94 million. Total, the corporate’s dividend is might face discount or elimination within the face of a extreme recession.

Alternatively, traders must be conscious that the dividend has remained basically flat over the past decade. Thus, it’s prudent to not anticipate significant dividend development going ahead.

Shares of Bridgemarq are at present buying and selling at 9.9 instances our anticipated earnings-per-share of $1.00 for 2026. We’ve assumed a good price-to-earnings ratio of 10.0 for the inventory. Reverting to our goal valuation by 2031 would add 0.1% to annual returns over this era.

Contemplating the 0.0% annual development of earnings per share, the 9.9% dividend yield, and a small tailwind from a number of enlargement, Bridgemarq might provide a 8.5% common annual whole return over the following 5 years.

Ultimate Ideas

Bridgemarq has a dominant place in its enterprise and enjoys pretty dependable money flows because of the recurring nature of most of its charges. It additionally gives an exceptionally excessive dividend yield of almost 10% which makes it enticing for income-oriented traders. The payout ratio is excessive, which might point out a possible dividend minimize if the enterprise fails to supply sturdy outcomes.

Given whole return potential and the opportunity of a dividend minimize in a downturn, we place a maintain score on shares of Bridgemarq Actual Property Providers.

Don’t miss the sources beneath for extra month-to-month dividend inventory investing analysis.

And see the sources beneath for extra compelling funding concepts for dividend development shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

")

")

")

{kind=link}