Up to date on April twenty second, 2026 by Josh Arnold

Actual Property Funding Trusts, or REITs, give buyers a hands-off technique to take part in actual property’s financial upside. They’ve grown in recognition over time as earnings buyers search different methods to generate portfolio earnings.

One facet impact of the rising recognition of REITs is the emergence of specialised REITs, which give attention to just one subsector of the true property business. For instance, Dream Workplace REIT (DRETF) is the biggest pure-play workplace REIT within the Canadian market, with a dominant place in workplace properties.

Dream Workplace inventory has a excessive 6.3% present dividend yield. And, its dividends are paid month-to-month, as a substitute of the standard quarterly payout. We observe that dividends are declared in Canadian {dollars}, so buyers within the US are inherently subjected to foreign money fluctuations consequently.

Month-to-month dividend shares are uncommon. You may obtain our full listing of all 119 month-to-month dividend shares (together with related monetary metrics like dividend yields and payout ratios), which you’ll be able to entry under:

The mixture of Dream Workplace REIT’s dividend yield and month-to-month dividend funds will certainly catch the attention of high-income buyers.

This text will analyze the funding prospects of Dream Workplace REIT intimately.

Enterprise Overview

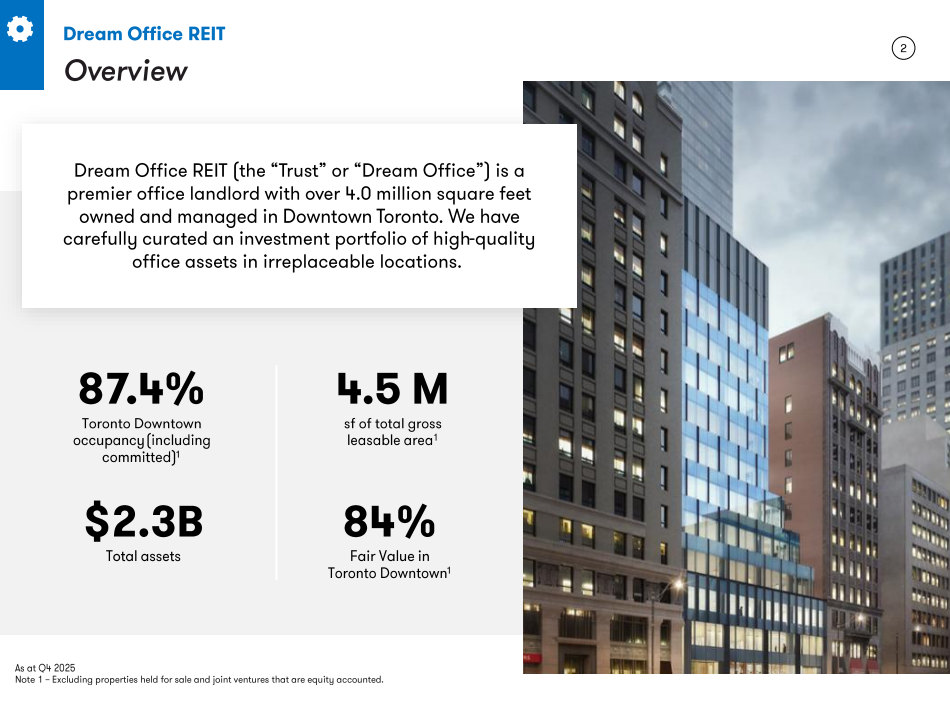

Dream Workplace REIT is an open-ended Funding Belief that acquires and manages predominantly workplace properties in main city areas all through Canada, however primarily in downtown Toronto. The belief has a market capitalization of $233 million at present market costs. It’s a part of the Dream Limitless household of actual property trusts, which additionally contains Dream Industrial REIT (DREUF).

Dream Workplace concentrates closely on workplace house properties in Toronto. Roughly 87% of its portfolio is in Toronto, and the rest is unfold throughout a number of markets.

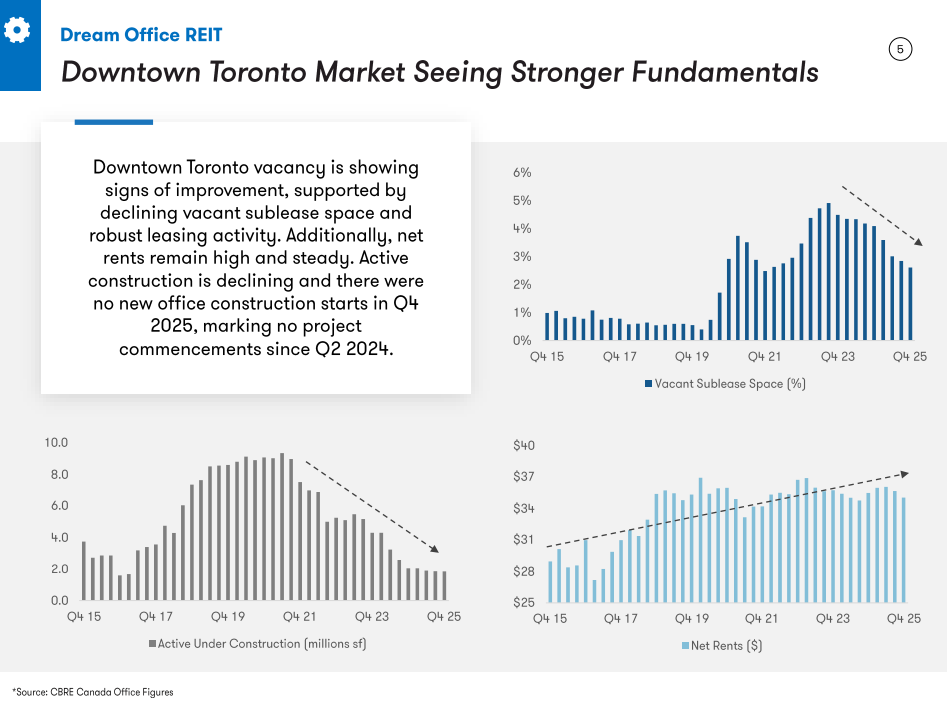

Toronto’s workplace house fundamentals are favorable, so Dream Workplace continues to pay attention its investments there.

Supply: Investor Presentation

This can be a important change from only a few years in the past when the portfolio was extra diversified. Dream Workplace has taken the daring step of considerably reducing its geographic diversification, nevertheless it has superb causes for doing so.

Toronto has tremendously robust fundamentals for workplace house, together with low (and declining) emptiness charges. This helps drive pricing larger and is why Dream has guess huge on Toronto. It additionally helps assist the values of its properties for when it comes time to divest a few of its holdings.

Dream Workplace posted fourth quarter and full-year earnings on February nineteenth, 2026, and outcomes had been blended. Web rental earnings was $19.1 million, down from $19.9 million within the year-ago interval. This was due primarily to the sale of the 438 College Avenue property, in addition to barely decrease occupancy in downtown Toronto following the expiry of the 74 Victoria Avenue property.

Similar-property web working earnings was up modestly to $17.7 million, as larger in-place rents and optimistic absorption in secondary markets helped offset decrease Toronto occupancy. The REIT accomplished 224k sq. toes of leasing exercise in the course of the quarter. New leases had been signed at common rents 2% under expiring ranges, as a consequence of weaker market circumstances. In-place occupancy completed the yr at 76.6%, with dedicated occupancy at 82.1%.

Diluted funds-from-operations per unit was 41 cents for the quarter, down from 53 cents a yr earlier. We count on $1.60 in FFO-per-share for 2026.

Progress Prospects

The surroundings Dream Workplace is working in stays difficult, and as such, we’re estimating zero earnings progress for the foreseeable future.

Dream’s progress prospects depend on excessive occupancy charges in Toronto and rising lease costs. The belief put in place a strategic plan to capitalize on its new focus in Toronto and make investments for the longer term. Below this plan, the belief offered billions of {dollars} of non-core property, shrinking its portfolio and producing money proceeds within the course of. It used this transformation to enhance unit pricing in addition to improve its publicity to downtown Toronto.

Supply: Investor Presentation

The end result has been a considerably smaller portfolio, however one which has a a lot larger lease base, permitting the belief to deleverage and afford it the power to scale back the belief’s share depend. This has not solely improved the stability sheet however its funds-from-operations per share as properly as a result of the share depend has dwindled.

In brief, whereas we don’t see Dream Workplace as producing enormous progress numbers within the coming years, it’s well-positioned to proceed to learn organically from larger base rents. Toronto’s workplace house fundamentals are adequate to assist this progress, regardless of near-term challenges.

Dividend Evaluation

Dream Workplace at present distributes a month-to-month dividend of C$0.0833 per share (C$1 per share annualized). This represents an annualized payout of roughly $0.73 per share in U.S. {dollars}, good for a 6.3% present yield.

Dream lower its distribution in 2017, and the payout has been relatively stagnant since then. Given the manageable payout ratio (anticipated at 43% for 2026), we don’t see a excessive danger of an additional lower as we speak. Nonetheless, we do stay cautious of the considerably shaky fundamentals within the workplace property market.

We at present count on $1.60 in FFO-per-share for this yr. The decline displays softer occupancy in comparison with final yr and better rates of interest, which can suppress the corporate’s profitability. Nonetheless, protection stays enough on the present dividend, so we don’t see additional cuts as mandatory. We reiterate the yield is kind of substantial at 6%+.

Be aware: As a Canadian inventory, a 15% dividend tax might be imposed on US buyers investing within the firm exterior of a retirement account. See our information on Canadian taxes for US buyers right here.

The 6.3% dividend yield is probably going excessive sufficient to entice earnings buyers. That is significantly true as a result of Dream pays shareholders month-to-month as a substitute of quarterly.

Last Ideas

Dream Workplace REIT’s excessive dividend yield and month-to-month dividend funds make it interesting to earnings buyers. Nonetheless, its long-term basic outlook is relatively unsure within the face of a rising price surroundings, and we see humble progress potential within the coming years. Moreover, shares seem overvalued at present costs, which might weigh on complete annualized returns.

The 2017 dividend lower looms massive for buyers, however the dividend yield is now fairly hefty following the inventory’s current weak point. Additional, the present payout is properly lined, and we view it as protected, even with softer occupancy ranges and rising curiosity bills. General, although, the inventory will not be very interesting presently as a consequence of a weak complete return potential.

Don’t miss the sources under for extra month-to-month dividend inventory investing analysis.

And see the sources under for extra compelling funding concepts for dividend progress shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}