Printed on April thirtieth, 2026 by Josh Arnold

Actual property funding trusts, or REITs, can supply extremely enticing revenue yields. They’re required to pay the vast majority of their earnings as dividends to their shareholders.

That is why many retirees and different revenue buyers prefer to put money into REITs, though not all REITs are equally well-liked. It could actually make sense to search for REITs outdoors of the US, as there are enticing and dependable dividend payers in different international locations as properly. This consists of RioCan Actual Property Funding Belief (RIOCF), for instance, which is a Canadian REIT.

RioCan REIT is a considerably particular REIT as a result of it pays month-to-month dividends. Whereas another REITs additionally pay month-to-month dividends, most supply quarterly dividend funds to their house owners.

There are presently simply 119 month-to-month dividend shares. You may obtain our full Excel spreadsheet of all month-to-month dividend shares (together with metrics that matter, like dividend yield and payout ratio) by clicking on the hyperlink under:

RioCan REIT affords a dividend yield of 5.5% at present costs, greater than 5 instances the S&P 500’s yield of 1%.

The above-average dividend yield and RioCan’s month-to-month dividend funds make the REIT worthy of analysis for revenue buyers. This text will talk about the funding prospects of RioCan REIT intimately.

Enterprise Overview

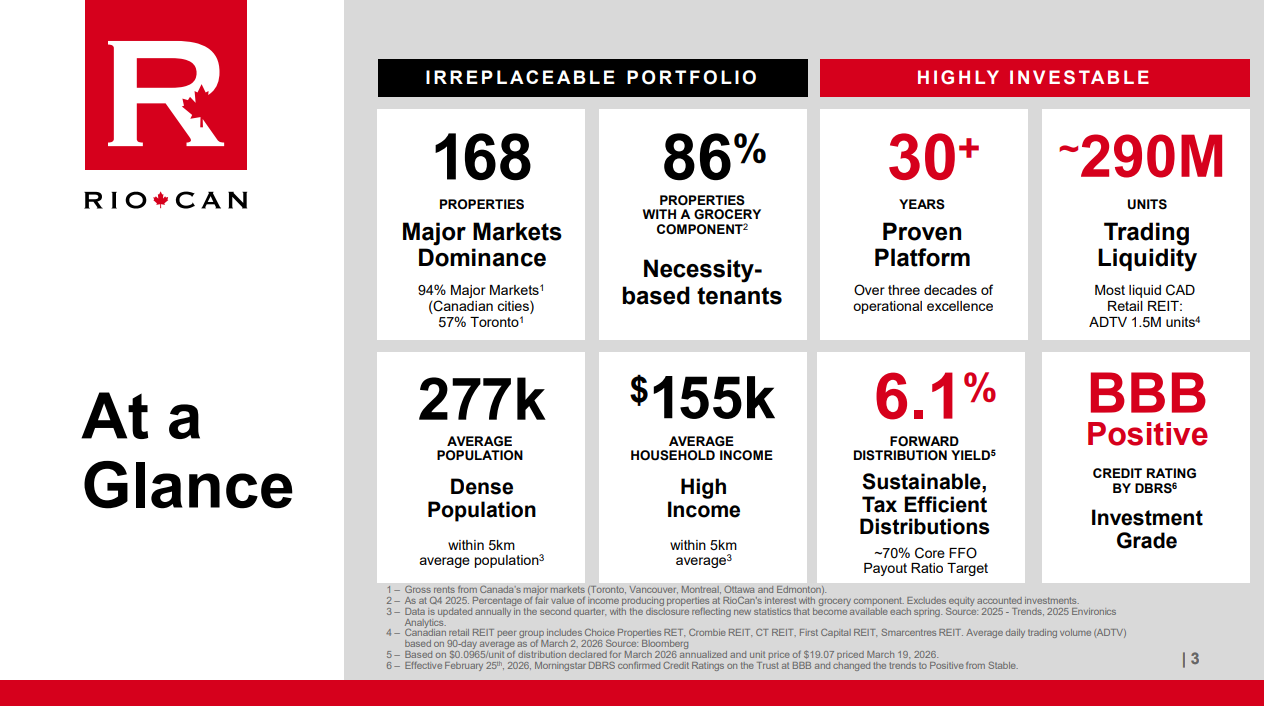

RioCan is an actual property funding belief that was based in 1993 by Ed Sonshine, making it one of many first REITs in Canada general. RioCan is headquartered in Toronto, Canada, and is without doubt one of the largest REITs within the nation. The corporate presently has a market capitalization of $3.5 billion.

The REIT invests in business properties with a retail actual property focus. Nonetheless, the corporate has been diversifying its asset base lately, which is why RioCan describes its portfolio as retail-focused and more and more mixed-use.

Among the REIT’s headline numbers might be seen right here:

Supply: Investor Relations

RioCan focuses on massive city markets, the place demand for properties is mostly larger, and common rents are larger as properly. Because of urbanization, persons are shifting into these markets, which is why the longer-term outlook for these properties is optimistic. Greater than half of its properties (by sq. footage) are situated within the Better Toronto Space.

RioCan owns practically 170 properties, with about 31 million sq. toes of web leasable space. On high of that, there’s an enormous pipeline of high-quality belongings that RioCan plans to develop over time amounting to about 17 million sq. toes, though this may take years.

Whereas retail REITs might be weak to recessions and different macro shocks after they have a deal with (lower-quality) malls the place tenants aren’t resilient, RioCan’s focus is completely different. Lots of its tenants are necessity-based, i.e. drug shops, grocers, and so forth. These have a tendency to stay resilient throughout recessions, which is why there may be little threat that RioCan’s tenants will default or run into bother in a giant means.

Underneath its RioCan Residing model, RioCan additionally affords residential actual property. Like within the business portfolio, the main focus right here is on high-class belongings within the largest and fastest-growing markets. Whereas common lease yields within the residential area are decrease relative to business belongings, residential actual property could be very resilient; thus, the buildout of this enterprise lessens a number of the threat with RioCan.

As well as, hire development within the residential area is larger than in lots of different actual property markets; thus, the residential enterprise might permit for an improved natural development charge sooner or later.

RioCan posted fourth quarter and full-year earnings on February seventeenth, 2026, and outcomes had been first rate. Income was up 3.5% year-over-year to $285 million through the quarter. FFO-per-share fell 5.1% year-over-year, whereas core FFO fell 4.7% for the quarter.

New leasing spreads had been 37.3% for the 12 months, whereas blended leasing spreads had been 21.1%. These mirrored continued robust provide and demand fundamentals for the belief’s properties. Business same-property web working revenue grew 4.5% for the fourth quarter, and three.6% for the 12 months. Complete capital repatriation was $742 million, whereas debt to adjusted EBITDA was all the way down to a still-elevated 8.6X. The belief additionally repurchased $179 million in its personal inventory.

We see $1.14 in adjusted FFO-per-share for 2026, largely consistent with 2025.

Development Prospects

RioCan has grown its funds from operations-per-share at a stable tempo prior to now and targets 5% to 7% annual FFO-per-share development within the coming years. We’re extra cautious, nonetheless, at 2.5% projected medium-term development.

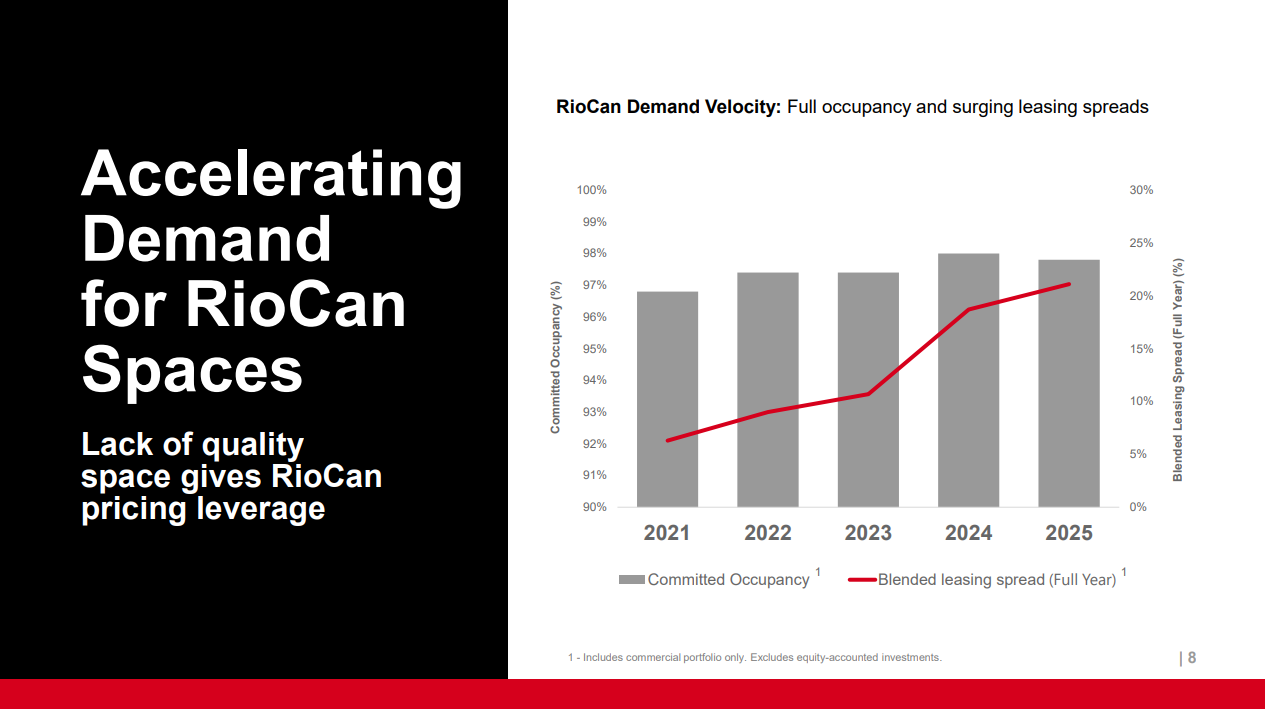

This funds from operations development was made attainable by a number of contributing elements. First, the corporate can enhance its same-property rents over time:

Supply: Investor Relations

We be aware that leasing spreads have been within the 5% to 10% vary per 12 months within the latest previous earlier than surging prior to now two years. Whereas leasing spreads will doubtless not be as excessive as the extent seen over the previous few years going ahead, it may be anticipated that RioCan’s high-quality belongings and underlying market development will permit for ongoing stable lease charge development at present properties. Rising rents at present properties permit for optimistic same-property web working revenue development, a vital driver for the corporate’s FFO.

Second, RioCan’s improvement pipeline and asset purchases ought to enhance the corporate’s money flows going ahead. RioCan targets a payout ratio of 55% to 65% of its funds from operations through dividends, which signifies that appreciable extra money is retained. That money can be utilized to finance the event of latest initiatives, whereas utilizing it for acquisitions is one other chance. It needs to be famous that it is a a lot decrease payout ratio than most of the month-to-month dividend-paying shares in our protection universe. We reiterate that the belief has been shopping for again shares as properly.

RioCan’s wholesome stability sheet additionally permits the REIT to finance a few of its future investments through debt. The corporate’s capital recycling exercise of promoting non-core belongings additionally generates money that can be utilized to pay for the event of latest and enticing properties in RioCan’s pipeline.

Dividend Evaluation

RioCan REIT is seen primarily as an revenue funding like many different REITs. And rightfully so, as the corporate affords a lovely dividend yield of 5.5%, primarily based on a month-to-month dividend payout of CAD$0.0965. On the present alternate charge to USD, shares of RioCan REIT are buying and selling at USD$15.47.

With FFO of USD$1.14 for 2026 and projected dividends of USD$0.85, the payout ratio is projected to be 74%. This means that the dividend is comparatively protected, as that’s not a excessive payout ratio for a REIT, as many friends function with a lot larger payout ratios.

When FFO retains rising per share, even in a tricky financial setting, there may be little motive to fret concerning the dividend as protection improves over time, all else equal.

The stability sheet additional signifies that there’s little motive to fret a few dividend minimize. RioCan’s debt to belongings stand at solely about half, which is comparatively conservative for a REIT.

Ultimate Ideas

RioCan REIT is one among Canada’s largest and oldest REITs that operates with a retail-focused portfolio however that has been increasing within the mixed-use and residential area lately. The REIT affords a lovely dividend yield of greater than 5%.

The deal with high-quality belongings in massive and rising markets signifies that RioCan’s portfolio is probably going positioned properly for the long term, as rents ought to proceed to climb over time, as they’ve finished prior to now.

With its robust high-quality asset base and a well-covered dividend, monthly-paying RioCan REIT has advantage as an revenue funding at present costs.

Don’t miss the assets under for extra month-to-month dividend inventory investing analysis.

And see the assets under for extra compelling funding concepts for dividend development shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

-1024x715.jpg?w=120&resize=120,86&ssl=1 "AG Nominee Todd Blanche Clears a Critical Congressional Hurdle")

{kind=link}