E-mini-Nasdaq 100 Futures reached a brand new all-time excessive of twenty-two,901.50 on Friday and are at present buying and selling close to these prior highs. See our earlier evaluation right here: Clear Path in the direction of New All Time Highs E-mini S&P 500 Futures are approaching their all-time highs, whereas Futures proceed to lag, at present down 3.73% year-to-date (YTD).

Supply: Finviz (As of 03:45 AM CT)

The ‘Yr-to-Date Efficiency’ knowledge exhibits a variety of asset behaviors. Notably:

- The USD is down 9.93% YTD.

- Power can be down YTD, contributing to inflation stabilization, although it stays above the Fed’s 2% goal.

- Valuable and industrial metals: Platinum, Palladium, , Gold, and Silver are among the many high performers.

- G10 FX futures have broadly outperformed the USD, with EUR main, up 12.06% YTD.

- market cap has recovered to its peak of $54.6 trillion.

Key Questions for H2 2025

What are the expectations for:

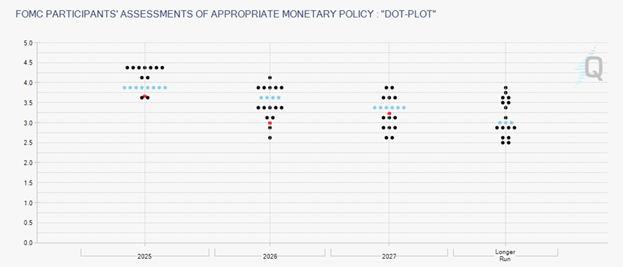

Federal Reserve’s June 2025 Dot Plot

Supply: CME FedWatch

Fed officers stay reluctant to chop charges, citing considerations about tariff-induced inflation probably rising within the coming months. In keeping with the dot plot, the median forecast suggests the federal funds price will fall to three.9% by year-end 2025, implying two 25 foundation level cuts.

Nevertheless, the outlook amongst officers is combined:

- 7 contributors anticipate charges to stay unchanged (up from 4 in March).

- 2 contributors anticipate one minimize.

- 8 contributors anticipate two cuts.

- 2 contributors foresee three cuts.

Expectations for price reductions in 2026 and 2027 are murkier and unsure.

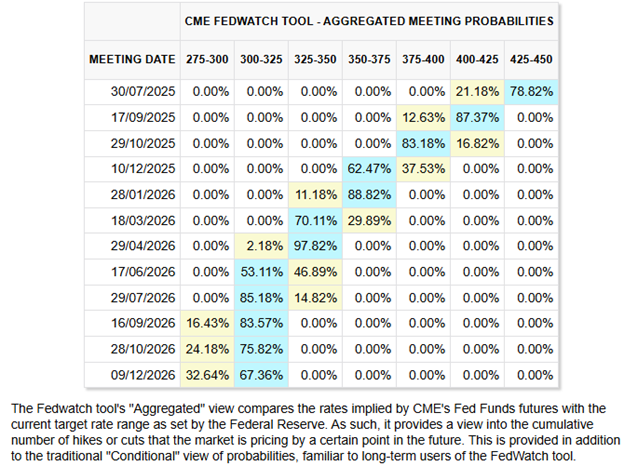

Market vs. Fed: Diverging Price Expectations

Supply: CME FedWatch

The CME FedWatch Device signifies that markets are pricing in:

- Two 25 bps cuts by October 2025.

- 65% likelihood of a 3rd 25 bps minimize by year-end.

- By end-2026, charges are anticipated to be round 3.00-3.25 % stage.

Notably, most Fed officers have adopted a extra hawkish tone forward of the July 2025 assembly besides Governor Waller. Market sentiment is more and more influenced by expectations that President Trump could appoint a extra dovish Fed Chair.

Morgan Stanley sees a better probability of no price cuts in 2025, with greater and extra cuts in 2026. They cite tariff induced inflation within the close to time period, with weaker client spending with a lag. They anticipate larger costs with tariffs translating right into a consumption tax. Stanley’s World Head of Macro Technique Matt Hornbach expects that the Fed will see extra inflation earlier than seeing a weaker labor market.

Authorities Debt and Financial Coverage Pressures

The price of debt service is now the third-largest authorities expenditure, a whopping $1.03 trillion surpassing protection spending. With U.S. nationwide debt exceeding $37 trillion (Supply: US Debt Clock), President Trump is advocating for decrease charges to facilitate refinancing at decreased prices.

Fed’s Up to date Financial Projections

- Actual GDP progress for 2025 has been revised right down to 1.4% (from 1.7% in March).

- The PCE inflation forecast was revised as much as 3.0% (from 2.7%).

These revisions level to stagflationary pressures, as each progress slows and inflation persists.

Fiscal Coverage: Trump’s BBB Invoice and Debt Implications

The Senate is about to vote right now on President Trump’s sweeping tax minimize and spending invoice, following a slim 51–49 vote to open debate. The Congressional Price range Workplace (CBO) estimates that the Senate model of the invoice would add $3.3 trillion to the nationwide debt over the following decade.

Though commerce offers are including to market optimism, many overlook that the efficient tariff price on China has reached 55%. The invoice’s passage might gasoline additional inflation whereas including to authorities debt. July ninth tariff deadline for a lot of nations approaches. Nevertheless, as beforehand famous, the worst is behind us and we anticipate Trump to not rooster out however reshape how tariffs are seen by combination contributors.

Key questions stay:

- Will larger tariffs translate into higher authorities income?

- Can reshoring manufacturing and home industrial coverage materially increase GDP?

The U.S. seems to be transitioning from globalization to strategic de-globalization, not full decoupling, however definitely a “Trendy Mercantilist” method echoing the time period cited by Bridgewater Associates.

Geopolitical Panorama

Center East:

A fragile Iran–Israel ceasefire holds. Nevertheless, dangers of preemptive strikes on Iran persist, notably contemplating IAEA Chief Grossi’s current assertion that Iran might resume uranium enrichment adequate for a bomb inside months (Supply: BBC).

Jap Europe:

No ceasefire has materialized between Russia and Ukraine. The battle is more likely to persist as Russia sees no profit in a ceasefire with out key calls for being met.

NATO Summit:

NATO members have dedicated to extend protection spending to five% of GDP, divided as follows:

- 3.5% for core protection.

- 1.5% for defense-related expenditures, together with help to Ukraine.

Progress on the 5% goal can be reassessed in 2029.

Asia:

China hosted the Shanghai Cooperation Group (SCO) summit with 10 member states, together with Iran, India, Pakistan, Russia, and Central Asian nations, specializing in regional stability and counter-terrorism efforts.

Closing Ideas

We’re clearly coming into an period of shifting alliances and multi-polar complexity. World order is evolving, and discerning reality from propaganda is more and more tough. For market contributors, value motion stays a essential information as markets typically value in new developments earlier than they attain the general public area.

***

Disclaimer: Derivatives buying and selling entails a considerable threat of loss. Previous efficiency isn’t indicative of future outcomes. Any instance trades aren’t inclusive of charges and commissions.

{kind=link}