Up to date on April thirtieth, 2026 by Nathan Parsh

Mullen Group (MLLGF) has two interesting funding traits:

#1: It’s providing an above-average dividend yield of 4.2%.

#2: It pays dividends month-to-month as a substitute of quarterly.

Associated: Record of month-to-month dividend shares

You possibly can obtain our full Excel spreadsheet of 119 month-to-month dividend shares (together with metrics that matter, like dividend yield and payout ratio) by clicking on the hyperlink under:

The mix of an above-average dividend yield and a month-to-month dividend makes Mullen Group interesting to income-oriented traders. As well as, the corporate is likely one of the largest logistics suppliers in Canada, with an immense community and powerful enterprise momentum. On this article, we’ll focus on Mullen Group’s prospects.

Desk of Contents

You possibly can immediately leap to any particular part of the article by utilizing the hyperlinks under:

Enterprise Overview

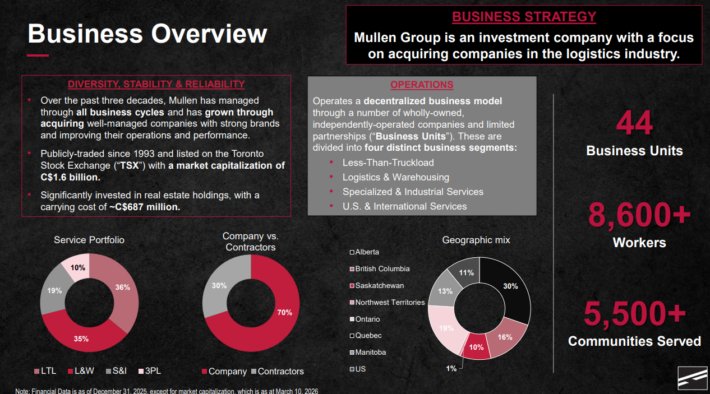

Mullen Group is likely one of the largest logistics suppliers in Canada. It began with only one truck in 1949 and has turn into an immense logistics supplier with 40 enterprise models. It’s headquartered in Okotoks, Alberta, Canada.

Its community of independently operated companies offers a variety of service choices, together with less-than-truckload, truckload, warehousing, logistics, transload, outsized, third-party logistics and specialised hauling transportation. As well as, the corporate offers numerous specialised providers associated to the power, mining, forestry, and development industries in western Canada, together with water administration, fluid hauling and environmental reclamation.

Mullen Group operates in 4 enterprise segments: Much less Than Truckload, Logistics & Warehousing, Specialised & Industrial Providers, and the U.S. & Worldwide Logistics phase.

The Much less Than Truckload phase is the biggest first and final-mile community in western Canada and Ontario.

Supply: Investor Presentation

This phase is tied to client wants and gives supply providers with managed temperatures all through the supply. It has 11 enterprise models, greater than 168 terminals, and greater than 5400 factors of service. This phase performs greater than 3 million deliveries yearly.

The Logistics and Warehousing phase has 11 enterprise models and is concentrated on North America.

Supply: Investor Presentation

This phase has roughly 20,000 subcontract vehicles and operates beneath an built-in expertise platform.

As a logistics firm, Mullen Group is delicate to the underlying financial situations and, therefore, susceptible to recessions. The corporate incurred a 22% lower in its earnings-per-share in 2020 because of the fierce recession and the provision chain disruptions brought on by the coronavirus disaster.

Nonetheless, because of the large distribution of vaccines worldwide, the pandemic has ended, and the financial system has recovered. Consequently, Mullen Group has absolutely recovered from the pandemic. It exceeded its pre-pandemic earnings in 2021 and posted 9-year excessive earnings-per-share of $1.20 in 2022.

On April twenty third, 2026, Mullen Group reported its first quarter outcomes on April twenty third, 2026. Income grew 10.2% to a report $399.8 million. EPS rose to $0.16 from $0.15 final yr, resulting from a change in margin enlargement, AI-led effectivity good points, and disciplined price controls amid weak progress and gas worth volatility.

Progress was pushed by current acquisitions, most notably the Cole Group, and powerful progress charges within the Logistics & Warehousing and U.S. & Worldwide Logistics segments. These good points had been partially offset by weak point in Specialised & Industrial Providers following the completion of non-recurring 2025 tasks, in addition to decrease LTL income ensuing from extreme winter climate and the strategic “demarketing” of particular clients.

Mullen is projected to earn $0.93 per share in 2026, which might be a 25.7% enchancment from the prior yr.

Progress Prospects

Mullen Group tries to develop its earnings in some ways. It seeks alternatives to broaden its community, optimize its current operations, and reduce prices to reinforce its working margins. General, administration has most well-liked enhancing working margins as a substitute of gaining market share in any respect prices.

Then again, the corporate has struggled at time to develop its earnings-per-share during the last decade. Foreign money trade has performed an element on this as the corporate is on the mercy of the worth of the Canadian greenback vs the U.S. greenback.

General, although, the corporate has skilled stable progress. In U.S. {dollars}, earnings-per-share have a compound annual progress price of seven.4% during the last 10 years and 9.5% during the last 5 years.

We forecast that the corporate can develop EPS at 3% yearly by way of 2031. .

Dividend & Valuation Evaluation

Mullen Group is at the moment providing an above-average dividend yield of 4.2%, practically 4 occasions the 1.1% yield of the S&P 500. The inventory is thus an attention-grabbing candidate for income-oriented traders, however U.S. traders must be conscious that the dividend they obtain is affected by the prevailing trade price between the Canadian greenback and the USD.

Mullen Group’s anticipated payout ratio for 2026 is 67%, which is wholesome. As well as, the corporate has a powerful steadiness sheet, with web debt of ~$660 million, which is about 50% of the inventory’s market capitalization. Consequently, the corporate is just not prone to reduce its dividend considerably anytime quickly.

Then again, you will need to observe that Mullen Group has considerably lowered its dividend during the last decade. To make certain, the corporate has provided a dividend of $0.61 in 2025, which is 48% decrease than the dividend of $1.17 that the corporate provided in 2013.

The numerous dividend discount has resulted from the depreciation of the Canadian greenback vs. the USD and a decline within the firm’s earnings-per-share amid risky enterprise efficiency. To chop an extended story quick, Mullen Group is providing a stable dividend yield, however it’s prudent for U.S. traders to anticipate minimal dividend progress going ahead.

In reference to valuation, Mullen Group is buying and selling at 16x occasions its anticipated earnings-per-share for the yr. Given the corporate’s robust enterprise mannequin and its risky efficiency report, we assume a good price-to-earnings ratio of 12.0x for the inventory. Subsequently, the present earnings a number of is larger than our assumed truthful price-to-earnings ratio. If the inventory trades at its truthful valuation stage in 5 years, then a number of contraction would cut back annual returns by 5.6% over this time period.

Contemplating earnings-per-share progress of three.0%, the beginning dividend yield of 4.2%, and a mid-single-digit headwind from a number of contraction, whole annual returns may very well be simply 1.8percentthrough 2031.

Last Ideas

Mullen Group has a dominant place in its enterprise because of its immense community. Nonetheless, the corporate has exhibited a risky efficiency report and has struggled at occasions to develop its earnings-per-share during the last 10 years. Subsequently, traders ought to make certain to determine a large margin of security earlier than investing on this inventory.

Mullen Group is providing a dividend yield of greater than 4%. The corporate has a stable payout ratio of 67% and a powerful steadiness sheet. Consequently, its dividend must be thought-about secure, although traders mustn’t anticipate significant dividend progress anytime quickly. General, the inventory appears greater than absolutely valued proper now, and therefore traders ought to look ahead to a extra engaging entry level in an effort to improve their future returns. Shares earn a maintain ranking consequently

Don’t miss the sources under for extra month-to-month dividend inventory investing analysis.

And see the sources under for extra compelling funding concepts for dividend progress shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}