Edited by Simisola Fagbola, Econoday Economist

The Financial system

Financial coverage

The Reserve Financial institution of Australia lowered its fundamental coverage price, the money price, by 25 foundation factors from 3.85 % to three.60 % at its assembly in the present day, according to the consensus forecast. This price was left on maintain on the RBA’s earlier assembly in July after it was minimize in April. The speed choice coincided with the publication of up to date financial forecasts within the quarterly Assertion on Financial Coverage.

Within the assertion accompanying the choice, officers pointed to current declines in inflation and famous up to date employees forecasts indicating that underlying inflation will proceed to reasonable to across the midpoint of the goal vary of two % to 3 %. Regardless of ongoing tightness within the labour market, officers famous that uncertainty over world commerce tensions signify a danger to family and enterprise spending.

Reflecting these issues, officers concluded {that a} price minimize was warranted in the present day however additionally they confused that the stay cautious concerning the outlook. They once more famous that financial coverage is properly positioned for them to “reply decisively” if exterior components weigh on home financial circumstances.

The choice {that a} price minimize is warranted displays the truth that officers stay assured concerning the inflation outlook. Headline inflation continues to be forecast to be 3.0 % at end-2025 and three.1 % at mid-2026, with the end-2026 forecast revised up barely from 2.8 % to 2.9 %. The forecast for the trimmed imply measure of inflation at end-2026 stays unchanged at 2.6 %. Each measures of inflation are forecast to be at 2.5 % mid-2027, down from 2.6 % beforehand.

Officers have additionally revised down their development forecasts. Australia’s financial system is now forecast to broaden by 1.7 % on the 12 months within the three months to December 2025, down from 2.1 % beforehand, and by 2.1 % within the three months to December 2026, down from 2.2 % beforehand.

Inflation

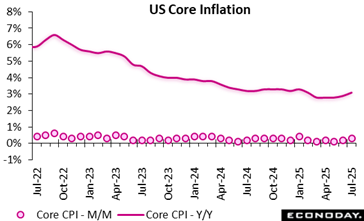

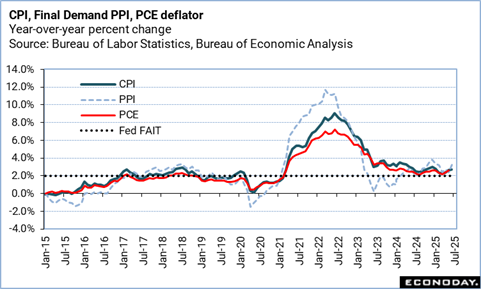

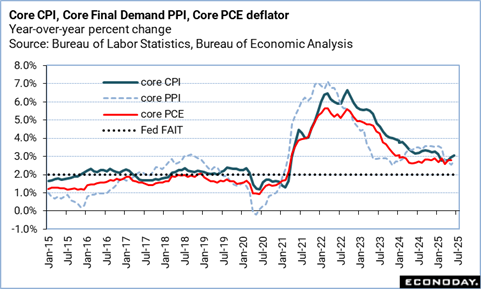

July’s US shopper worth inflation studying is benign on the floor however comprises indicators beneath of the anticipated inflationary results of upper tariffs. For instance, costs for furnishings, photographic gear, autos rose on a month-to-month foundation on the quickest price since April or Could. Nevertheless, the truth that the influence just isn’t extra widespread may enable the Fed higher confidence to decrease rates of interest in September.

The Client Value Index in July slowed to +0.2 %, following a 0.3 % rise in June, and a 0.1 % uptick in Could. The July CPI studying matches expectations for a 0.2 % rise within the Econoday survey of forecasters. This marks a return to the slower month-to-month tempo of total shopper worth inflation seen between February and Could.

During the last 12 months, shopper costs are up 2.7 %, matching the two.7 % year-over-year rise in June. Expectations within the Econoday survey had been for a 2.8 % enhance.

Core CPI, excluding meals and vitality costs, is up 0.3 %, after rising 0.2 % in June, and +0.1 % in Could. Client costs much less meals and vitality jumped 3.1 % from July 2024, following a 2.9 % year-over-year rise in June, and three % anticipated within the Econoday survey.

After rising by 0.2 % in June, shelter prices rose by 0.2 % in July (and are up 3.7 % year-over-year). Meals costs had been flat, after a 0.3 % bounce in June, with grocery costs down 0.1 % final month, and restaurant costs rising 0.3 %.

Vitality prices contracted by 1.1 % over the month, following a 0.9 % spike in June – dragged down by a 2.2 % fall in gasoline costs.

Vitality costs are down 1.6 % year-over-year, following a 0.8 % dip for the 12 months ending June. Meals costs elevated by x % in comparison with July 2024, following a 3 % rise in June.

Employment

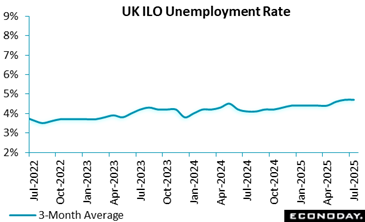

The UK labour market in mid-2025 confirmed that payrolled staff declined by 149,000 over the 12 months to June and an extra 164,000 by July, signalling subdued hiring momentum. Whereas the employment price for 16–64-year-olds rose to 75.3 %, unemployment edged as much as 4.7 %, suggesting extra individuals are actively in search of work. Financial inactivity fell to 21.0 %, hinting at a gradual re-entry into the workforce.

Vacancies fell for the thirty seventh consecutive interval, down 44,000 to 718,000, with most industries reporting fewer openings, reflecting attainable warning amongst employers about recruitment or substitute hiring. Wages continued to develop robustly, with common earnings up 5.0 % and better within the public sector (5.7 %) than within the personal sector (4.8%), whereas whole earnings together with bonuses, had been 4.6 %. Actual pay development remained modest at 0.9% (CPIH-adjusted), indicating inflation’s lingering squeeze on family buying energy.

In the meantime, the Claimant Rely fell to 1.695 million, providing a counterpoint to softening payroll numbers. Nevertheless, 38,000 working days had been misplaced to labour disputes in June, underscoring ongoing tensions in pay and circumstances. Total, the information recommend a labour market in transition, holding regular in employment charges however going through persistent recruitment warning and wage-price pressures.

GDP

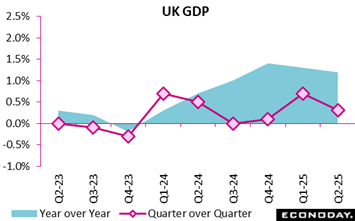

The UK financial system maintained its development trajectory within the second quarter of 2025, with GDP rising by 0.3 %, following a stronger 0.7 % growth within the first quarter. In contrast with the identical interval in 2024, GDP grew by 1.2 %, reflecting regular however moderating momentum.

In output phrases, providers, the UK’s dominant sector, expanded by 0.4 %, whereas development posted strong development of 1.2 %, underscoring resilience in infrastructure and constructing exercise. Nevertheless, manufacturing contracted by 0.3 %, highlighting continued pressures in manufacturing and associated industries.

Actual GDP per head grew by 0.2 % within the quarter, and by 0.7 % year-over-year, indicating that output features had been modest as soon as inhabitants development was factored in. Importantly, no revisions had been made to beforehand printed GDP figures, with extra complete information updates scheduled for August and September 2025 below the Nationwide Accounts Revisions Coverage.

Total, the second quarter efficiency factors to a gradual, service-led financial system bolstered by development, however tempered by weak spot in manufacturing.

Demand

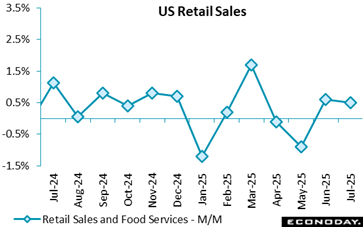

U.S. retail gross sales got here in as anticipated in July whereas June’s studying was revised increased. The underlying information is a combined bag, with contractions in some sectors with an publicity to tariffs, however sufficient spending resilience in classes like autos, in addition to division and furnishings shops. Sufficient shopper resilience for Federal Reserve officers to stay affected person concerning the timing of the following price minimize.

U.S. July retail gross sales jumped by 0.5 %, constructing on the revised 0.9 % month-to-month surge reported for June (beforehand +0.6 %), and as anticipated by the consensus within the Econoday survey of forecasters.

Nevertheless, core retail gross sales, eradicating autos and gasoline gross sales, solely elevated 0.2 % final month following a revised up 0.8 % studying in June (beforehand reported as +0.6 %). Core retail gross sales are up 4.4 % on an annual foundation in July in comparison with a 4.6 % y/y bounce in June.

Auto gross sales rose 1.7 % in July, following June’s 1.6 % enhance, and are up 4.9 % vs. final 12 months. Exercise continues its restoration after dwindling following the pre-tariffs spike in March.

Summer season spending is stable, however there gross sales contracted in sectors with publicity to increased tariffs. Constructing supplies, backyard gear and suppliers’ gross sales fell 1.0 % in July, electronics and home equipment had been down 0.6 %, and miscellaneous retailer retailers noticed a 1.7 % contraction.

E-commerce gross sales slowed barely to a 0.8 % enhance in July from +0.9 % in June, and they’re 8.0 % increased than a 12 months in the past.

In comparison with a 12 months in the past, July retail gross sales are up 3.9 %, in comparison with June’s 4.4 % bounce.

Excluding gasoline, retail gross sales elevated 0.5 %, after June’s 0.9 % enhance, and jumped 4.5 % from July 2024 vs. +5.0 % on an annual foundation in June.

Stripping out purchases of motor autos and elements, gross sales rose 0.3 % in comparison with a 0.8 % enhance (beforehand +0.5 %) in June. On an annual foundation, retail gross sales ex-autos are up 3.7 %, a slight slowdown from June’s 3.8 % tempo.

Sentiment

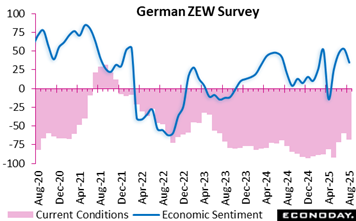

Germany’s financial temper darkened in August 2025, with the financial sentiment indicator plunging to 34.7, down 18 factors from July. This marks a break within the months-long upward development, reflecting rising unease amongst monetary market consultants. The present scenario evaluation slid additional into destructive territory at minus 68.6, pushed by weak second quarter efficiency and sector-specific pressures.

The not too long ago introduced EU–US commerce deal, as an alternative of boosting confidence, sparked disappointment. Considerations centre on its restricted advantages for key German industries, significantly chemical compounds, prescription drugs, mechanical engineering, metals, and automotive, already grappling with subdued demand.

The broader eurozone outlook mirrored Germany’s downturn. Financial sentiment fell to 25.1, a drop of 11 factors, with the present scenario index declining to minus 31.2. Downward revisions to development expectations underscore that the slowdown just isn’t confined to Germany however extends throughout the financial union.

In essence, August’s outcomes reveal a fragile restoration overshadowed by commerce deal skepticism, persistent industrial headwinds, and a softening eurozone outlook, portray an image of cautious optimism giving technique to renewed concern.

Enterprise Surveys

US Evaluation

CPI and PPI-FD Present Import Value Pressures Rising

By Theresa Sheehan, Econoday Economist

The patron worth index (CPI) and final-demand producer worth index (PPI-FD) for July each recommend that worth pressures are beginning to swing increased. Digging by means of the information, it’s pretty clear that costs are going up in classes associated to imports. New tariffs and consequent efforts by companies to recoup the prices have gotten extra seen. It’s much less apparent within the July CPI numbers, however the PPI factors to rising costs on the shopper stage in coming months.

This isn’t surprising. What stays in query is how a lot of the prices will shoppers be requested to pay, how massive these prices are, and the way lengthy will it take to move by means of the inflation information? Upward worth pressures are evident for commodities and providers, and are broad-based. Nevertheless, it’s within the meals and vitality classes that customers are prone to really feel the best discomfort.

If costs for meals had been unchanged within the CPI index for July from June, the PPI for last demand meals is up 1.4 %. The CPI for vitality was down 1.1 % in July from the prior month, however the PPI vitality index exhibits a 0.9 % enhance. These commodities have a direct and instant influence on family incomes and spending.

The providers utilized by households are many and diverse. The influence of worth modifications is tougher to parse out. Nonetheless, service companies typically have little selection however to move on prices to prospects. The CPI for all providers was up 0.3 % in July, whereas the PPI for last demand providers is up 1.1 %. A few of that is prone to present up in transportation the place passenger carriers and shippers generally enhance charges to maneuver items and ship providers.

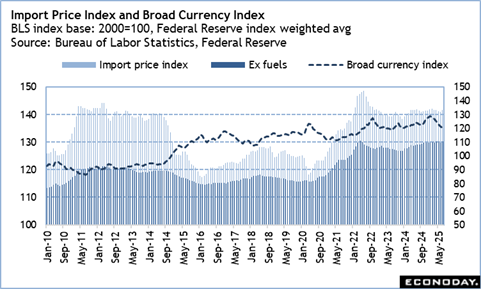

The import worth index for July exhibits a 0.4 % enhance from the prior month, though it’s down 0.2 % year-over-year. The index for imported fuels – that are priced in US {dollars} – is up 2.7 % in July, and down 12.1 % year-over-year. The import worth index for nonfuels is up 0.3 % in July and 0.9 % increased than a 12 months in the past. Partially, the weaker US greenback versus a broad basket of currencies means imports are getting costlier.

Titans")

")

{kind=link}